Introduction

China has made strategic choices favouring renewables over fossil fuels that are still not widely understood or appreciated. Hao Tan and I have been making these arguments for several years now, and in particular in our article in Nature in September 2014 we argued that China had overwhelming economic and energy security reasons for opting in favour of renewables, in addition to the obvious environmental benefits.1 In this article I wish to take these arguments further and update the picture to incorporate comprehensive 2015 data as well as fresh targets for 2017 and 2020. The context is China’s continuing battle to scale back its use of coal; its imminent release of the country’s 13th FYP for Energy, based on the overall 13th FYP for economic development over the five years 2016 to 2020, where new renewable energy targets will be announced or consolidated [See ChinaDialogue]; and China’s hosting of the G20 meeting in Hangzhou in September, where it will be promoting an international drive for greening of finance – with China itself playing a key role in this process. China is becoming a major promoter of international infrastructure development, in Africa and across Central Asia through the One Belt-One Road strategy – and this too carries strong implications for other countries’ energy choices.

The 2015 results

The first task is to review the results for China’s electric power system in 2015, to check that the leading edge of the system is still greening faster than it is becoming black – as Hao Tan and I have demonstrated for previous years. And it’s clear that the 2015 data do indeed support this trend. While the electric power system is just one industry, it is a large one and traditionally a heavy user of coal. And the strategic direction it takes carries over to the rest of the economy. So using the electric power system as proxy for the economy as a whole (it is the largest consumer of coal), the full data are given in Table 1, covering the three aspects of electric power generated, electric generating capacity added, and investment in new generating facilities.

Table 1. Power generation and changes, China, 2014-2015

|

1. Generation TWh |

||||||||

|

2014 |

2015 |

Change |

Change |

Share of total system |

||||

|

TWh |

% |

% |

||||||

|

TOTAL |

5,546 |

5,600 |

54 |

1.00% |

||||

|

Thermal |

4,173 |

4,077 |

-96 |

-2.30% |

73.00% |

|||

|

Water |

1,066 |

1,110 |

44 |

4.10% |

19.40% |

|||

|

Wind |

156 |

185 |

29 |

18.6% |

||||

|

Sun |

23 |

67 |

43 |

191.0% |

4.70% |

|||

|

WWS subtotal |

1,246 |

1,362 |

116 |

9.30% |

24.60% |

|||

|

Nuclear |

126 |

161 |

35 |

27.8% |

2.90% |

|||

|

2. Capacity GW |

||||||||

|

2014 |

2015 |

Change |

Change |

Share of total system |

||||

|

GW |

% |

|||||||

|

TOTAL |

1,360 |

1,507 |

147 |

10.70% |

||||

|

Thermal |

915.7 |

990.2 |

74.5 |

8.00% |

65.7% |

|||

|

Water |

302 |

319 |

17 |

4.90% |

||||

|

Wind |

95.8 |

130 |

34.2 |

33.40% |

||||

|

Sun |

27 |

41 |

14 |

52.00% |

||||

|

WWS subtotal |

424 |

490 |

66 |

15.60% |

32.5% |

|||

|

Nuclear |

20 |

26 |

6 |

29.90% |

1.7% |

|||

|

3. Investment US$ billion |

||||||||

|

2014 |

2015 |

Change |

Change % |

|||||

|

Green energy |

94 |

110 |

16 |

17% |

||||

|

Source: Based on China’s primary sources: National Bureau of Statistics (NBS) and National Energy Agency (NEA) |

||||||||

First, in terms of electric power generated, we find that total electric power generated by China in the year 2015 was 5,600 TWh (or billion kWh) – making China’s electric power generation by far the highest in the world. This total is flattening out, indicating that China is decoupling its energy consumption from economic growth. Each year the proportion of electricity generated by thermal sources (fossil fuels) declines; it reached just 73% in 2015 (meaning that non-thermal sources, mostly renewables, account for 27% of the electricity generated). In fact, the power generated from thermal sources actually declined in absolute terms in 2015, down to 4,077 TWh – a decline of 96 TWh, or by 2.3% compared with the year before – and this for the second year in a row. By contrast, power generated from pure renewables (water, wind and sun) increased in 2015 by 116 TWh, to reach 1,362 TWh – up 9.30% on the year before. So power generated from thermal sources declined in absolute terms in 2015, while power generated from water, wind and sun increased. This is the clearest possible evidence that the leading edge of the electric power generating system is greening. Nuclear sources also accounted for an extra 35 TWh, to reach 161 TWh – still a long way behind WWS (Water, Wind and Sun) pure renewable sources.

Of course the system as a whole is still largely black – that’s what 73% dependence on fossil fuels means. But the trend, the leading edge, is definitely headed in a green direction. Over the past decade, dependence on thermal sources reached a peak of 83.3% of power generated in the two years 2006 and 2007, and has been declining each year since to reach just 73.0% in 2015 – or a 10% decline in a decade. This is a remarkably swift shift for such a large technical system – particularly one that is growing rapidly – and is the basis for targets that see thermal sources accounting for just 63% by 2020 and less than 50% by 2030. By this time the total electric power system in China would be greener than blacker. The implications of these trends and data for coal consumption and carbon emissions will be discussed below.

Second, in terms of generating capacity the same shift in a green direction can be detected, if less strongly. Total electric power generating capacity reached just over 1.5 TW by 2015 – again, by far the largest in the world (compared with the US total of just 1 TW). In terms of capacity added in 2015 (i.e. where the system is changing), thermal sources added 74.5 GW, while water, wind and sun sources added 66.3 GW and nuclear a further 6.2 GW, making non-thermal sources adding 72.5 GW – so that thermal sources added marginally more than non-thermal sources in the year. It is the sub-totals that are of most interest, with China adding world records of 32.5 GW wind power in 2015 (to reach a cumulative total of 130 GW) and 14.6 GW of solar power, to reach a cumulative total of 41.1 GW – both totals being by far the largest of any country in the world, and growing faster than in any other country.

In terms of capacity added, 66% came from thermal sources in 2015 and 32.5% from water, wind and sun, plus 1.7% from nuclear, or 34% from non-thermal sources – more than a third. This demonstrates clearly how large the Chinese commitment to non-thermal sources of electric power has become. Now as in the case for 2014 data we have an immediate issue to explain in these statistics, which is how a system that adds thermal power capacity in 2015 (albeit at a low rate) can actually generate less power from these sources than in the previous year. The answer is consistent with the explanation given by Tan and myself in 2014, namely that much of the thermal power capacity being added is actually not being utilized in generating electricity.

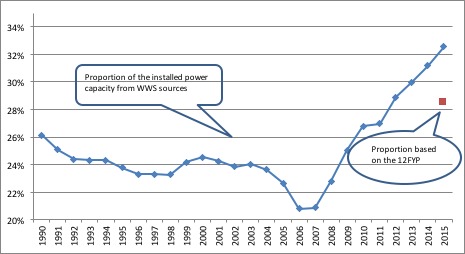

When we look at trends in capacity being installed, we see another strong trend in China towards the green outranking the black. As noted for the 2015 results discussed above, there is a significant change in China’s energy patterns headlined by a strong shift towards the use of renewables, namely electric power generation from renewable sources such as wind, solar PV and water (hydro). This is captured in the changing proportions of power generated from WWS sources vs power generated from thermal sources in terms of capacity – as shown in Fig. 1.

|

China: Trends in power sources generated from Water, Wind and Sun, 1990 to 2015 Source: JM/HT based on Chinese sources |

Chart 1 demonstrates a clear change in direction in China’s electric power system – with WWS generating capacity rising from a low of just 21% in the years 2006 to 2007 to reach 32.5% in 2015 – or more than a 10% increase in a decade. This is a rapid shift in the fundamentals of the electric power system – with China demonstrating to other industrial and industrializing countries that the green shift is feasible and that it can deliver economic, social and environmental benefits.

So the trends in terms of capacity are very clear. The total capacity for water, wind and sun in 2015 reached, as we have seen, no less than 490 GW power – very nearly half a trillion watts of clean power. According to official targets, the total is set to rise to 550 GW in 2017 (330 GW for water, 150 GW for wind and 70 GW for solar). And by 2020 the targets specify 740 GW (made up of 340 GW for water, 250 GW for wind, and 150 GW for solar PV). Note that these are realistic targets, consistent with previous rates of growth and with the additions for 2015. If China is indeed generating renewable power at 740 GW in 2020 it would be the world’s undisputed renewables superpower – and one that is well on the way to becoming the world’s first country to become a terawatt renewables powerhouse (generating in excess of 1 TW or 1000 GW) by early in the 2020s – less than a decade from now.

Thirdly, the trends in terms of investment show a similar greening tendency outstripping the tendency towards blackening, or adding further coal-fired sources to the energy system. China’s investment in renewables sources of electric power in 2015 reached a world record of $110.5 billion – mostly going on wind farms, solar farms and hydro dams (including smaller hydro facilities, not just giant dams). According to Bloomberg New Energy Finance (BNEF), China’s investment of $110 billion accounts for no less than 33% of the global green investment of $329 billion in 2015 – itself a world record total. China’s investment matches the combined total of the next two industrial powers, namely the US ($56 billion) and the EU ($58.5 billion).

The contrast with investment in thermal generating capacity is striking. According to China’s National Energy Administration, China invested 139.6 billion yuan (around US$21 billion) in new coal-fired power stations in 2015. This is less than a fifth of the investment in clean energy sources. In the same briefing on the electricity sector in China in 2015 the NEA revealed that investment in hydro amounted to 78.2 billion yuan (or US$11.7 billion) and in nuclear power investment was 56 billion yuan (or US$8.4 billion). So it is safe to say that China’s green investment in renewable power sources in 2015 well surpassed investment in thermal sources. This is a third indication that the leading edge of the electric power system is greener than blacker. The most arresting feature of China’s greening of investment in energy in 2015 was the introduction of green bonds as a major source of finance – a point to be returned to in a moment.

Overall trends

Continuing coal dependence

The first point to acknowledge is how enormous China’s coal-based power system is, and how it continues to spew out carbon emissions as well as other greenhouse gases such as methane. There is as well the particulate pollution that so ruins the air in China’s big cities. China burns far more coal than any other country – indeed, as much as the rest of the world combined. This is the price that China has paid, and is paying, for its breakneck industrialization through which it is catching up with the industrially advanced world.

While China is reducing its consumption of and reliance on coal each year, it nevertheless burns a lot of coal and will continue to do so for many years to come. When Hao Tan and I last examined this issue we noted the rapid increase in approvals for new coal-fired power plants being issued by provincial governments – but more recent moves by the national agencies including the NEA seem to have reversed these trends, and China is now on a path to permanently reducing its coal production and consumption, and coal imports, in favour of progressively greater reliance on green energy sources. Some commentators now project that China’s carbon emissions could peak by 2020 – a full decade earlier than commitments made by China in UN climate gatherings and as part of the US-China Climate Agreement reached in 2014.

China’s ‘black’ energy system is certainly still black – although it is greening at the edges, as shown clearly in Fig. 2. Here it can be seen how China’s thermal generation of electricity increased rapidly (the black bars) particularly after 2001 when China joined the WTO and was ‘open for business’. But the last two years have seen a decline in thermal power generation from the peak reached in 2014. Coal consumption overall and coal consumed in power generation are shown as continuous lines, where again there was a marked increase after 2001 for the first decade and a half of the 21st century, followed by a plateau and then absolute decline in 2014 and 2015.

|

China’s “black” energy system, 1980-2015 Source of primary data: The data for conventional thermal electricity generation is available from the China Electricity Council (CEC); the data for total coal production is available from the BP Statistical Review (2016) ‘Statistics of World Energy’; the data for coal consumption for thermal power generation is available from the National Bureau of Statistics, China. |

This is the ‘black face’ of China that is responsible for so much particulate pollution, making the air in cities like Tianjin and Beijing unbreathable. Indeed China’s coal consumption fell in 2015 to reach just over 4 billion tonnes. Coal production actually peaked in 2013, and has been falling ever since. Even more dramatically China’s coal imports fell in 2015 by 30%. Coal imports fell to 204 Mt in 2015, down from 291 Mt in 2014 – a drop of 30% in a year. And this trend can be expected to continue. The National Energy Administration (NEA) announced in 2015 that it would not approve any more coal-fired power stations, effectively putting them under a moratorium for the next three years.

The levelling off in coal consumption around 2012/2013, with coal consumption actually falling in the years 2014 and again in 2015, is striking. It reveals the power exercised by governments in China, both national and provincial, to intervene in the economy to drive things in a new direction. This is an important advantage enjoyed by China.2 On the other hand, there have been reports of provincial governments deliberately intervening to support their coal-fired power plants at the expense of wind power installations. The Chinese Wind Energy Association has pointed to the Yunnan provincial government issuing a policy that imposed a surcharge on wind and hydropower producers and used the revenue to subsidize coal-fired plants; a similar arrangement was reported from the Xinjiang provincial government.3

At the same time we see that China has been building its green energy system as complement to the black, coal-fired system during a transition period. Taking wind power as the prime case, Fig. 3 demonstrates how China’s wind power capacity has been rapidly built out, doubling every three years or so since 2007.

|

China wind power capacity, 2000-2015 Source of primary data: BP (2016) Statistics of World Energy |

Note that this chart underestimates China’s real growth in wind power, as revealed by the official Chinese figures reproduced in Table 1. But we may use the data from the BP Statistics report as this is widely accepted.

The scale of China’s build-up of green energy capacity is only appreciated when compared to what other countries are doing. Fig. 4 shows the situation in terms of capacity to generate power from water, wind and sun, in 2015, comparing different industrial countries.

|

China’s generation capacity from WWS sources compared with other leading industrial countries, 2015 Source: JM/HT, based on REN21 (2016) Global Status Report. Note that the total WWS capacity for China is listed as 496 GW, as per the REN21 report, whereas the revised Chinese statistics utilized above indicate that the figure should be 490 GW encompassing water, wind and solar. |

It is worth comparing China’s investments in green energy with the EU, making it clear that China has already caught up and is now in the lead. Drawing on data from BNEF and Xinhuanet, the London-based consultancy E3G published a chart revealing the widening gap between China and the EU. China invested over $110 billion in clean energy in 2015 (as we have seen), compared with just $40 billion for the EU – outranking the EU 2.5 times. China’s investment overtook that of the EU in 2013, and has strengthened its lead each year since then – while EU investment has actually declined. Per capita investment by China also overtook that of the EU in 2015, while China’s investment in clean energy as a proportion of its GDP has already reached 1% — compared with less than 0.3% for the EU.4

|

Clean energy investment, China vs EU, 2005 – 2015 Source: E3G Note that ‘Total investment in clean energy’ refers to investment for the relevant year in all renewable energy sources. |

Given this comparative dominance of China in building green energy infrastructure, it is all the more remarkable that international agreements such as the OECD-sponsored pact to limit subsidies for the export of coal-fired power stations (reached in the weeks prior to the Paris Climate deal of December 2015) leave China out of account.5 Such omissions become increasingly untenable as China’s international influence rises.

China’s manufacturing strategy

Hao Tan and I have been at pains to emphasize that China has made a strategic choice in favour of renewables not (just) for reasons of mitigating climate change and reducing particulate pollution, but also (and probably more importantly) in terms of energy security. This is to be guaranteed by China’s strategic choice to manufacture all the devices needed for its renewable energy generation.

With solar panels, for example, China has been building up its manufacturing capacity rapidly, moving to a position of world leadership in 2007 – a full decade ago – as shown in Fig. 6.

|

Manufacturing of solar PV panels, by country, 1995-2015 Source: pv magazine |

The chart shows that China moved rapidly to world leadership by 2007, and to securing more than 50% of global output of solar panels by 2011. Now under the impact of trade sanctions brought against Chinese manufacturers, the companies like Trina Solar expanding into Thailand and Canadian Solar expanding into Vietnam are globalizing their activities, further cementing their leadership.

A similar story can be told for wind power, where again China has been building a strong national wind turbine manufacturing capacity, alongside its build-up of wind farms. By the year 2015 there were five Chinese firms in the world’s top ten wind turbine producers, with Goldwind emerging for the first time as the world’s number #1 producer.

China’s rapid expansion of manufacturing in wind turbines is reflected in the 2015 results for the world’s Top 10, with Chinese firm Goldwind emerging as world #1, followed by Danish firm Vestas and US firm GE in third place. [See “China overtakes EU to become global wind power leader”] [See also “Chinese wind turbine maker is now world’s largest”]

In 2015 Goldwind received orders for 7.8 GW of new turbines, followed by Vestas with 7.3 GW of new orders and GE with 5.9 GW of new orders. Four other Chinese firms ranked amongst the world’s top 10 – Guodian, MingYang, Envision and CSIC (Fig. 7).

|

The Top 10 Wind Turbine Manufacturers in 2015 and their global market shares Source of primary data: REN21 (2016) Global Status Report |

Greening of finance

Behind these trends towards a greening of China’s energy system lies the power of finance – in this case, state-directed finance mediated via development banks. China is emerging as a leader in the financial aspects of the process of greening, driven by an appreciation of the crucial role of finance if ambitious investment strategies are to be successful. Brought together by Dr Ma Jun of the People’s Bank of China, the Green Finance Task Force in China issued its long-awaited report ‘Establishing China’s Green Financial System’ in April 2015 – making China the first country in the world to set specific guidelines for the issuing of green securities.6 The report sets out an ambitious agenda for how China can green its rapidly developing financial and capital markets, making use of policy, regulatory and market-innovations. The report notes that China will need investment each year of at least 2 trillion yuan (US$320 billion) or more than 3 percent of GDP, for at least the next five years if it is to achieve its green targets.7

China’s banks are already moving into this new space for the issuance of green bonds. The Agricultural Bank of China was the first Chinese financial institution to do so, raising $1 billion from a three-part green bond in October 2015.8 The green bond market in China is set to grow significantly as the government there has given the go-ahead to banks to launch large issues. The Shanghai Pudong Development Bank came out with a green bond worth 20 billion Yuan (US$4.3 billion) in January 2016. In its cautious but determined way, China is moving towards a quota for banks totalling 300 billion Yuan (more than US$45 billion) in green bond issues.9 Thus the year 2015 has seen a decisive shift towards serious greening of finance, with China playing a significant role in this process.

As against these positive trends in greening of finance, it is also important to acknowledge that the year 2015 saw a considerable expansion of China’s development bank financing of infrastructure around the world, including new coal-fired power developments and fossil fueled projects in Africa, Central Asia and elsewhere. China’s ‘black’ energy economy is now internationalizing through the activities of China’s development banks, now the largest source of development finance in the world.10

Counter trends

While emphasizing the greening trends in this article, there are of course counter-trends that also need to be noted. As fast as China is adding solar and wind power to its national grid, the connection of these sources to the grid, and, as in many other countries, its capacity to accept input from fluctuating energy sources, is still limited. Curtailment of wind power contributions reached a high level in 2015, with cumulative wind power capacity reaching nearly 130 GW but only 100 GW of this supplying power to the grid.

The fact is that China is leading the world in upgrading its grid to make it stronger and smarter. The world’s largest electric utility, the State Grid Corporation of China (SGC) is now moving ahead with advanced plans to build long-range Direct Current power lines that lose less power during transmission than their AC counterparts. And the SGC is investing heavily in its grid upgrading activities. On the international front, the SGC is advancing its support for and promotion of the North East Asian Grid, connecting China, Mongolia, Japan, Korea and Russia. This is seen by the SGC as a means of enlarging the scope for renewable power to be utilized by the grid, and as a step towards the proposed Global Energy Interconnection, SGC’s most ambitious project to date. [See the book outlining the proposal]

No one really knows whether China’s efforts to green its economy and extend its greening efforts to the North East Asian Grid, for its own very practical economic and business reasons as much as for environmental reasons and reasons based on climate change considerations, will succeed. The commitments of decades towards the black, fossil-fueled system have been so enormous, and backed by powerful efforts to create a world class fossil fuel system that could mine, drill and transport huge quantities of coal, oil and gas to China’s fast-expanding manufacturing industry. Now the environmental and social price of this huge build-up has become clear, and China’s leadership is moving as rapidly as it can to change energy direction – with the results in 2015 indicating just how far these efforts are taking the country. But whether it will eventually prove to be sufficient, to save China and the world, is an open question.

References

Green, F. and Stern, N. 2016. China’s changing economy: Implications for its carbon emissions, Climate Policy

Mathews, J.A. and Tan, H. 2016. Circular Economy: Lessons from China, Nature, 331 (24 March 2016): 440-442.

Related articles

John Mathews and Hao Tan, The Revision of China’s Energy and Coal Consumption Data: A preliminary analysis

Andrew DeWit, Japan’s Bid to Become a World Leader in Renewable Energy

John Mathews and Hao Tan, A ‘Great Reversal’ in China? Coal continues to decline with enforcement of environmental laws

John A. Mathews and Hao Tan, The Greening of China’s Black Electric Power System? Insights from 2014 Data

John A. Mathews and Hao Tan, “China’s Continuing Renewable Energy Revolution: Global Implications”

John A. Mathews and Hao Tan, “Jousting with James Hansen: China building a renewables powerhouse”

John A. Mathews, The Asian Super Grid

Andrew DeWit, Japan’s Energy Policy at a Crossroads: A Renewable Energy Future?

Sun-Jin YUN, Myung-Rae Cho and David von Hippel, The Current Status of Green Growth in Korea: Energy and Urban Security

Notes

I would like to acknowledge the generous assistance that Dr Hao Tan has provided in the preparation of this article – as in other works where we have collaborated.

See the paper by Green and Stern (2016) making this point with regard to China’s dramatic turn to clean sources of energy.

See ‘China’s wind power conundrum’, Greenbiz, 11 July 2016, at: https://www.greenbiz.com/article/chinas-wind-power-conundrum

See the E3G report ‘Pulling ahead on clean technology: China’s 13th Five Year Plan challenges Europe’s low carbon competitiveness’, by Shinwei Ng, Nick Mabey and Jonathan Gaventa (March 2016), available at: https://www.e3g.org/docs/E3G_Report_on_Chinas_13th_5_Year_Plan.pdf For commentary on Europe’s poor showing in investment in clean energy, and its likely implications, see the story in The Guardian, 23 March 2016, at: https://www.theguardian.com/environment/2016/mar/23/european-clean-tech-industry-falls-into-rapid-decline

See reports on this OECD-sponsored pact such as “OECD agrees deal to restrict financing for coal technology”, Eur-Active.com, 18 November 2015, at: http://www.euractiv.com/section/energy/news/oecd-agrees-deal-to-restrict-financing-for-coal-technology/

See the report at: https://www.cbd.int/financial/privatesector/china-Green%20Task%20Force%20Report.pdf

The figure of 2 trillion yuan is a broad figure referring to investment in green industries generally; it is not a specific target as embodied in the 13th Five Year Plan. Nevertheless it is the first time that a government has been specific about the scale of investment needed to make the green transition.

See the Reuters report, at: http://www.reuters.com/article/china-bonds-offshore-idUSL3N12E1N620151014

See the report at: http://cleantechnica.com/2016/01/25/two-chinese-banks-set-issue-green-bonds-worth-15-billion/

See the recent study by Kevin Gallagher and colleagues from Boston University’s Global Economic Governance Initiative, in collaboration with Yongzhong Wang of the Chinese Academy of Social Science’s Institute for World Economics and Politics, ‘Fueling growth and financing risk: The benefits and risks of China’s development finance in the global energy sector’, available at: https://www.bu.edu/pardeeschool/files/2016/05/Fueling-Growth.FINAL_.version.pdf