This paper documents the fact that distributed power is a rapidly expanding and quickly evolving market with important implications for Japanese and global energy futures. It also shows that Japan has an excellent opportunity to grow a robust and sustainable business area that includes primary, secondary and tertiary industries. Distributed power can improve equity, local resilience, and build a more competitive export sector. But Japan may be handicapped by Galapagos features as well as the capacity of vested interests to block progress in power deregulation and other aspects that favour the diffusion of distributed power and efficiency. These handicaps may become even more pronounced after the December 16 general election, which is shaping up to be – at least in part – a contest over whether to stick with centralized power in the hands of Tepco and other giant utilities or accelerate the distribution of opportunities. The election seems likely to bring on even worse political confusion and gridlock than Japan endures at present, which will almost certainly advantage the status quo.

Distributed Versus Centralized Power

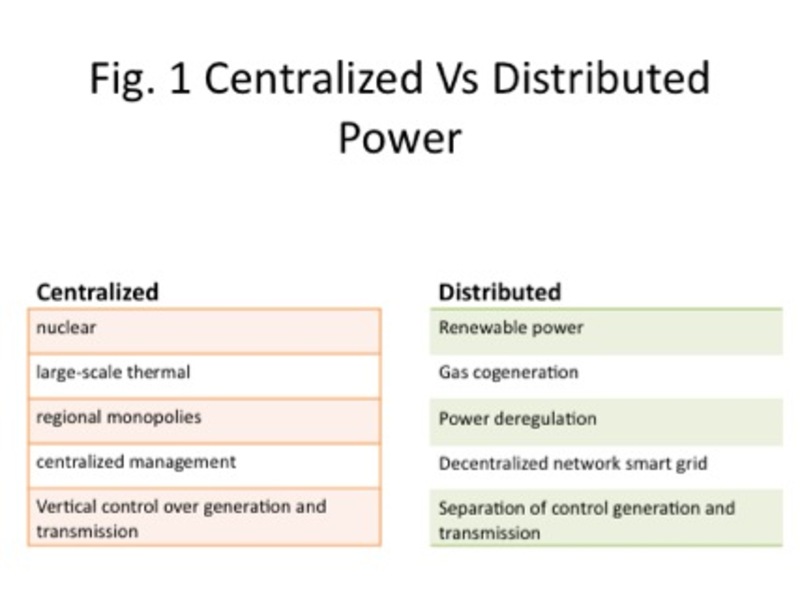

First, let me define distributed power. As we see from Figure 1, distributed power is the alternative to the centralized monopolized structure that currently dominates Japanese power markets and concentrates economic opportunity in monopolized utilities. Distributed power features smart grids, micro-grids and other advanced interactive technologies deployed on a local scale to network distributed renewable power generation. As “distributed power” implies, it distributes power-generation opportunities – via solar, wind, geothermal, biomass, and other means – to households, farmers, small businesses, local communities, and other interests.

The role of biomass is not confined to distributed power. Biomass has an increasing role in distributed energy, as we see in the production of sustainable biofuels. It is also finding an increasingly important role in the so-called “bioeconomy” in general. This contribution to sustainability is evident for example in the substitution of conventional hydrocarbon (i.e., coal, oil and natural gas) with bio-resources.1

Let us, however, focus on power. Centralized power generation, as in the fleet of nuclear reactors and the monopolized utilities, features very large-scale, conventional power generation infrastructure and a relatively low-tech, inflexible grid network. Some benefits accrue to local communities that host large-scale power generation plants, but these direct benefits are for the most part restricted to the utilities, their suppliers, and their work forces.

|

As for the size of the distributed power market, we see in Figure 2 that its cumulative value to 2030 was assessed as ¥3100 trillion by Nikkei BP. This assessment, compiled in early 2010, was based on extrapolations from a survey of 100 of 300-400 smart city projects then underway. The assessment centres on the energy storage opportunities that are a critical element of balancing supply and demand in power systems. Given the spread of smart and distributed power to a wider range of communities than was the case just two years ago, the assessment is quite likely to be a significant underestimate.

In any event, to get an appreciation of the scale of those growth numbers, consider that the Japanese economy’s annual GDP is roughly ¥500 trillion. That means the cumulative smart market, as projected by Nikkei BP, is at least six times the economic size of Japan. To establish a significant presence in that market means not just jobs for technicians, big firms, and the usual suspects, but rather a widely distributed array of interests. We have already seen this distribution of opportunity unfold in Germany, Denmark, and other locales.2

The Nikkei BP analysts themselves recognize the limitations of their survey in a rapidly evolving context. They add that the overall market is expected to increase to a cumulative ¥5000 trillion by 2030, “if markets in the related fields are included in the calculation, such as water infrastructure, smart housing, smart home appliances, operation and maintenance of the smart city equipment and devices, and services to visualize power consumption. The industries involved will be extensive, from manufacturing industries, such as electricity, electronics, and automobiles, to IT and communications, construction, and services, not to mention electricity and infrastructure.”3

This assessment, then, tells us that the smart and distributed power market encompasses the full range of industries, including primary, secondary and tertiary sectors.

|

Fig 2. Projected Size of Japan’s Distributed Power Market to 2030 |

Fuji Keizai also reported on November 22 of this year that it projects smart city markets in Japan to grow from 2011’s ¥1.1 trillion yen to ¥1.47trillion in 2012 (a 33.6% jump) and to ¥3.80 trillion by 2020 (the latter, a 340% expansion from 2011).4

Why Now?

There are a lot of reasons distributed power and smart infrastructure is gaining in attractiveness. Smart distributed power can reduce greenhouse gas emissions, power loss through long-range transmission (which is implicit in centralized power), accelerate technological development, and stimulate the growth of entire new industries and jobs in a sector that is melding energy, IT and biotech (roughly 20% of the average industrialized economy). Another reason for the spread of distributed power is that the distribution of power networks enhances the resilience of local communities in the face of natural disasters that literally put their lights out. When centralized power assets run into trouble, as they do much more frequently than many people imagine, a very large amount of generation capacity goes off-line. We saw this through the meltdown (or “melt-through”) of nuclear-reactor assets in Fukushima, in the wake of the March 11,2011 disaster and in New York City’s Sandy disaster of October 27, 2012.

Japan has significant efforts ongoing in growing distributed power. In January of this year, its cutting edge eco-model cities, such as Kitakyushu and Yokohama, were selected for a new program of “environmental future city” initiatives. The future city effort balances the best of the eco-model cities with the devastated Tohoku cities and smaller communities, as we see in the chart below.5 These projects are major, central-state sponsored initiatives to deploy the infrastructure of distributed power.

|

Fig 3. |

But there are many other initiatives. For example, Metropolitan Tokyo is installing distributed power in order to bolster its own resilience in the face of disasters. This power generation and grid network, which is being supplemented with renewable generation as well, is aimed at maintaining essential transport and other functions in the event of a repeat of last year’s large-scale power outages. It is also aimed at “blowing a hole” in Tokyo Electric’s business model, which is of course centralized and monopolized power generation and distribution.6 Kawasaki City and a slew of other urban centres are taking similar initiatives.

The Fukushima disruption to power supplies and the threat of continued instability indeed led most local governments and the central agencies that work with them to ramp up their spending on renewable energy, efficiency, storage in other means of producing, reducing, and retaining energy and power. The fiscal 2012 budgets for the central agencies as well as for the prefectures and the designated cities (such as Sendai with populations of 500,000 or more) show the scale of this spending. Expenditures on renewables, efficiency, storage, next-generation vehicle support, and related items totaled ¥202 billion for central agencies and ¥88.7 billion for the prefectures and designated cities.7

These numbers do not capture the total of local efforts. One reason is the locals have since implemented supplementary budgets. The locals and their central-agency sponsors are also organizing special finance packages for small and medium-size enterprises as well as other local actors (farmers, households) so they can benefit from installing renewable energy as well as energy efficiency. These finance packages include special low-interest loans and other forms of encouragement. They also offer tax exemptions and other special measures to attract renewable investment, encourage its diffusion among local residents, and the like.

These distributed power initiatives were greatly amplified by the July 1 introduction of the feed-in tariff, or FIT. As we see in the figure below, the feed-in tariff is a mechanism whereby the extra cost of producing renewable power is paid by customers of the utilities. It is important to emphasize that (except in a very few cases, such as the now defunct Korean feed-in tariff) the public sector does not transfer money to renewable producers. Even many experts misunderstand this fact.8 Rather, the public sector sets a premium price for renewable power depending on the generation type, assumed costs, and other factors. The government thenobliges the utility topurchase renewable power from properly designated renewable producers, including households, and mandates the utility to pass the extra cost on to consumers through their electricity bill.

|

Fig 4. |

At present, Japan has some of the highest renewable tariffs in the world, especially for solar projects. These prices are guaranteed for 20 years for megasolar, wind and small-hydro, and for 10 to 15 years for other projects such as household solar and geothermal.9 What this feed-in tariff structure does is guarantee a stable market and a stable price for what is, in general, currently more expensive power than conventional forms of power generation.

Naturally, there has been a flood of rhetoric from vested power interests and their allies in the business community about the costs of this feed-in tariff. But Japan’s Agency for Natural Resources calculates the additional costs as likely to be ¥70 to ¥100 per month for the average household.10

The feed-in tariff not only encourages the diffusion of renewable power capacity through guaranteed markets and prices. A properly designed feed-in tariff also includes scheduled declines in tariff prices, called degression rates. These are meant to encourage reductions in cost, and they work as we see from the following comparison of solar costs and diffusion in German, Japan and the US.

Though some observers express doubts about the wisdom of deploying the feed-in tariff, it has incentivized the German power economy to move from just under 8% renewables in 2002 to over 25.97% in the first half of this year. The country’s current targets for renewable power are 35% by 2020 and 80% by 2050.11

|

Fig 5. Installed photovoltaic capacity [Cumulated at year-end in GW] x Year |

Japan had a feed-in tariff, limited to solar, prior to the July 1 introduction of the new tariff that includes wind, small hydro, biomass, and geothermal as well. Until Fukushima, the Japanese power community had sought to use the feed-in tariff for their own purposes, to help supplant some reliance on fossil fuels while moving the core of the power economy towards 50% reliance on nuclear. This was a provisional compromise worked out in the pre-Fukushima collusive energy policymaking circles.

Large utilities that rely on centralized generation tend to dislike renewable energy because it is distributed. It simply does not fit into their business model. They and their investors want stability, in order to maintain their income streams from assets whose lifetimes are measured in decades. The more renewable power there is, distributed on household roofs and unused farmland, the smaller the market for the big utilities and the tougher their challenge in managing the grid and maintaining nuclear power facilities. This has been a political and technological challenge almost everywhere, especially in Germany and particularly at present.12

Redefining Power Options in Post-Fukushima Japan

In the wake of Fukushima, Japan’s renewable feed-in tariff was redefined in the political debate. The feed-in tariff went from a means of reducing reliance on fossil fuels to include displacing reliance on nuclear power. This expansion of the purpose of the feed-in tariff was strongly shaped by the efforts of Softbank’s CEO SonMasayoshi as well as former prime minister Kan Naoto. Kan got the FIT passed by the Diet on August 26 of last year. Kan and Son were key actors in diffusing awareness of the feed-in tariff as well as altering its purpose. Their initiatives have helped encourage an extraordinary level of mobilization at the local level and throughout the country. For example, Softbank CEO Son contributed to this mobilization by starting his Natural Energy Council last May. It now includes 39 of 47 prefectures as well as 18 of 20 designated cities. The councils also include 208 private firms.

This deliberate organization to foster the diffusion of renewable energy opportunities continues to be replicated throughout the country at the subnational level. There are a host of new councils, agencies, study groups and the like that focus on specific renewables or extend across the various types of renewables. Spatially, some of them stretch across prefectures, uniting entire regions, while others work within prefectures or within local communities. Some of them extend among local communities while others group various categories of resident such as citizens, farmers, small business, and the like. The rapid proliferation in the number of these renewable-energy associations came in tandem with the post-Fukushima multiplication of local organizations to foster resilience as well as exchanges of personnel among local communities.

This is the good news. Japan is in the midst of a distributed power revolution. The revolution is bonding innovative capital with SMEs, farmers, households, finance and other sectors. It offers a robust and sustainable growth option to a country that is otherwise greatly disadvantaged by ageing, a shrinking economy, woeful prospects for most women and younger workers, a scarcity of disruptive agency in an economy dominated by comparatively ossified interests, and other fundamental problems.

And Now for the Bad News

There is, at the same time, a great deal of bad news. One item is the likely fruits of the election on December 16, which seems almost certain to bring more political confusion and allow the monopoly utilities and their allies in government and the bureaucracy to revive the pre-Fukushima energy plan. This plan, which aimed at over 50% nuclear in the power mix by 2030, actually remains the de jure law.

It is impossible to project what will happen in the wake of the election. As of this writing, it even remains unclear how many parties will contest it, as the official start of the campaign is not until December 4. But it does not appear that Japan will find itself with a majority government, particularly a government willing to take on vested interests in the power sector as the three leading parties have all backtracked from earlier plans for closing the nuclear power sector. Quite the contrary. Yet Japan desperately needs good governance to, among other items related to distributed power, decide on feed-in tariff digression rates as well as deregulation of the power sector. It seems unlikely to get it.

Other bad news is the patent fact of accelerating climate change and its various effects.13 This should ramp up the demand for distributed power because resilience, or adaptation, is being added to the need for mitigation. One salient example: When hurricane Sandy hit New York last month, it wreaked havoc on the centralized grid. Specialists quickly noted that coops and other institutions with distributed power maintained lighting and heating functions.14 This fact, in the region that is the core of contemporary capitalism, has made distributed power even more an item of interest than it was prior to the shock.

It is useful, in this respect, to keep in mind that America is already very advantaged by a military committed to distributed power. The US Navy aims at 50% renewables by 2020, and the Defence Department overall at 25% by 2025.15 On November 28 of 2012, the military successfully fought off Senate advocates for vested energy interests, continuing its robust programmes for sustainable biofuels, such as algal-derived fuel.16 It also uses feed-in tariff-like policy (long-term contracts but not higher prices) to attract private investment in wind, solar and other renewable energy for its bases.17 The military rejects pressures from conventional energy interests, including nuclear,18 because – in its own warped way – it has come to understand the costs of unsustainability. Among a range of green initiatives and agencies, that defy the denialist mentality still prevalent among much of the US political class, the US Navy has for several years had an activist office of “Energy, Environment and Climate Change.”19 The Navy, and the other services of the US military, is also explicitly committed to leading an energy revolution.20

The point is not to tout the US military. But its emphasis on distributed power may provide a better indicator of where we are going, in the power economy, than the assessments of the International Energy Agency (IEA) and other international bodies or associations that represent conventional energy.21 These agencies draw up detailed reports that have to balance contending interests in the context of multiple crises and an industrial revolution. The results are often merely a snapshot of the prevailing common sense at a particular time rather than a sound, unbiased assessment of actual energy options.

For example, the IEA, the world’s premier energy agency, relegated renewable energy to a marginal role until early this year.22 This shift in the IEA’s position on renewable energy followed years of absurdly minimalist projections of per annum growth in wind and other renewable generation when observable reality showed levels many multiples higher.23 One reason for the shift was that, from 2006, the Energy Watch Group,24 a coalition of scientists and parliamentarians, began a sustained critique of the IEA and other agencies’ analyses. The bias in the IEA, towards the oil, gas and nuclear industries, was so obvious that the critique was akin to shooting fish in a barrel.25 In the wake of that episode as well as the emergence of the competing International Renewable Energy Agency (IRENA) on January 26 of 2009, the IEA began adding staff with specialization in renewables.26

Even so, the IEA’s numbers remain suspect. Its “World Energy Outlook 2012,” released on November 12, 2012, contains a number of suspect projections on oil production, the role of technology in solving escalating water-energy problems, expectations for carbon capture and storage, and the like.27

Here, I highlight the US military because of its spearhead role in distributed power and energy. In the protracted fight over sustainable biofuels with vested interests in Washington, it performed a critical political role in driving transformation.28 But perhaps it is also important to suggest that when the military are more responsive to economic and environmental reality than the political class and global energy analysts, we would appear to be in deep trouble indeed.

Resilience as Adaptation

In short, I am suggesting that there is an accelerating interest in distributed power and smart grids because of the increasing awareness of vulnerability and an expanding paradigm of resilience, and not just in Japan, as opposed to the assumed efficiency of large-scale, centralized power generation.

The speed at which this awareness is growing is difficult to capture empirically. But one indicator is the increasing capacity to measure the water-energy nexus, which is illustrated in the figure below.29

|

Fig 6. |

The figure illustrates that the water-energy nexus is a very complex phenomenon. But for our purposes here the collision between water and energy has become particularly manifest in the reliance on thermal power, which includes nuclear as well as gas and coal, on water for a variety of functions and especially for cooling. Due to climate change and other factors, it is becoming increasingly difficult to use conventional power in many areas. As early as 2003, in the European heat wave that killed tens of thousands, French nuclear reactors that relied on river-water for cooling functions had to be shut down even as demand for electricity increased. They had to be shut down because the flow of water decreased and its temperature increased making it impossible to use it for cooling without damaging the river as an ecosystem once the hot water was released into the rivers. This phenomenon is becoming increasingly common, and in summer 2012 at the Millstone reactor in Connecticut, on the Atlantic Coast, seawater was too warm to provide the level of cooling required, so the reactor had to be shut down for 12 days. By contrast with nuclear and other centralized generation technology, renewables and other distributed-power technologies have minimal demand for water. The figure below compares the various generation types’ reliance on water in terms of US gallons per megawatt of power generated.30

|

Fig 7. |

In August of this year, the Swedish Environmental Institute (SEI) released its combined LEAP (LEAP: Long range Energy Alternatives Planning System) and WEAP (Water Evaluation And Planning System) software, in a new version WEAP 3.3. As is evident from the screenshot of the software in the figure below, it is the ultimate in geekishness. But it is also a powerful tool, used in over 190 countries by thousands of organizations, which will now allow local, regional and national managers to see the linkage between energy and water. As the SEI describes it, WEAP 3.3 adds “the ability to link seamlessly with SEI’s energy and climate mitigation planning software, LEAP, for integrated analysis of water-energy trade-offs (the “nexus”). Used together, the two systems can model evolving conditions in both water and energy systems and show the cross-sectoral impacts of different policy choices.”31 This empirical demonstration of an increasingly constraining factor, for which there is no substitute, is almost certain to further drive markets in the direction of distributed power.

More bad news is seen in the competitive handicaps of the Japanese distributed power, smart market, especially the tendency towards Galapagos. This problem has been studied intensively by Mizuho Group, Fujitsu and others. They note that there is a relative scarcity of low-cost products and of products with a strong position in global markets. Moreover, they suggest it is a challenge to fit Japanese firms’ otherwise quite good technology with the needs of Asian and other customers.32

|

Fig 8. |

|

Fig 9. |

Now insert the water-energy nexus. Japan does not have a significant water-shortage problem for cooling its nuclear and other large-scale generation capacity. But a lot of its custumers and competitors do, and these problems appear to be worsening. The competitors are thus getting powerfully incentivized to innovate.

That hardly means that Japan is out of the running. The country enjoys a significant commitment to research and development, as shown in the chart below.33

But in the increasingly critical area of energy research, Japan seems significantly handicapped by the weight of vested interests. As we see from the figure below, fully 55% of Japan’s 2010 Energy RD&D budget is locked up by the powerful commitment to centralized and large-scale nuclear power. This very high number compares unfavourably with a 33% nuclear share in France, 31% in Germany, 19% in the US, and 17% in Brazil. Japan is clearly devoting far too much of its resources to an energy option that seems unlikely to be the wave of the future. In the wake of Fukushima the “nuclear renaissance” everywhere has lost momentum– save at the level of rhetoric – in the face of stiff competition from renewable and gas-fired power that is distributed. Nearly half of the nuclear build that is being undertaken in the world is going on in China, and, in part for political reasons, Japan seems very poorly placed to enjoy a significant role in that business.

There are a host of nuclear safety and other issues in Japan, of course. But one additional concern in this regard is that centralized nuclear capacity may undermine incentives to develop and deploy distributed power. That certainly seems to be one reason that Japan has so little renewable power installed (about 3% of power, compared to Germany’s 26%), even though it was once a renewable leader and has no significant endowments of conventional resources. Japan risks losing yet more ground in global markets to competitors who are more responsive to price and other signals. In short, there is a patent risk of becoming even more of a galapagos stuck in a centralized, nuclear-centred power economy while distributed and renewable-centred power is where nature’s signals appear to be pointing.

|

Fig 10. |

This paper has taken a critical look at the centralized versus distributed power paradigms and how they relate to post-Fukushima Japan’s opportunities. As we have seen, Japan has a fair amount of distributed power investment underway, accelerated by the feed-in tariff. Less clear is weather the country will continue pursuing this option as rapidly and avidly as it’s the growing number of competitors. Centralized, large-scale power generation would appear to have peaked as a paradigm, due to technological and market developments that increasingly undermine its 20th century economy of scale advantage. It is also challenged by the water-energy nexus, the need for resilience, and the other advantages of distributed power. Japan’s monopolized utilities and its big power-unit makers, like Hitachi and Toshiba, appear desperate to ignore this trend.34 One wonders if, in the Japanese case, something is going on that is comparable to GM’s in-house fight between SUV and hybrid/electric engineers during the 1990s, when the former won out and nearly wrecked the company.35

Andrew DeWit is Professor in the School of Policy Studies at Rikkyo University and an Asia-Pacific Journal coordinator. With Iida Tetsunari and Kaneko Masaru, he is coauthor of “Fukushima and the Political Economy of Power Policy in Japan,” in Jeff Kingston (ed.) Natural Disaster and Nuclear Crisis in Japan.

Recommended citation: Andrew DeWit, “Distributed Power and Incentives in Post-Fukushima Japan,” The Asia-Pacific Journal, Vol 10, Issue 49, No. 2, December 3, 2012.

Articles on related subjects:

• John A. Mathews, The Asian Super Grid http://japanfocus.org/-John_A_-Mathews/3858

• Andrew DeWit,Japan’s Energy Policy at a Crossroads: A Renewable Energy Future?

• Jeff Kingston,Japan’s Nuclear Village

• Andrew Dewit,Japan’s Remarkable Energy Drive

• Andrew DeWit,Megasolar Japan: The Prospects for Green Alternatives to Nuclear Power

• Peter Lynch and Andrew DeWit,Feed-in Tariffs the Way Forward for Renewable Energy

• Andrew DeWit,Fallout From the Fukushima Shock: Japan’s Emerging Energy Policy

• Sun-Jin YUN, Myung-Rae Cho and David von Hippel,The Current Status of Green Growth in Korea: Energy and Urban Security

• Son Masayoshi and Andrew DeWit,Creating a Solar Belt in East Japan: The Energy Future

• Kaneko Masaru,The Plan to Rebuild Japan: When You Can’t Go Back, You Move Forward. Outline of an Environmental Sound Energy Policy

• Andrew DeWit,The Earthquake in Japanese Energy Policy

• Andrew DeWit and Sven Saaler,Political and Policy Repercussions of Japan’s Nuclear and Natural Disasters in Germany

• Andrew DeWit and Iida Tetsunari,The “Power Elite” and Environmental-Energy Policy in Japan

Notes

1 The merger of information technology, energy and biotech is especially evident in the emergence of the so-called bioeconomy, which the EU is aiming at to help achieve sustainable reduction of its dependence on fossil fuels not just for fuel but as inputs into such materials as plastic, medicines, fertilizers, and the like. The bioeconomy has been assessed at 9% of EU employment (22 million jobs) and EURO 2 trillion in economic output. On this, see European Commission, “Bioeconomy – ensuring smart green growth for Europe,” no date: here

2 On the role and benefits of local ownership of power-production in Germany, Denmark and elsewhere, see Stephen Lacey, “Why Local Ownership of Renewable Energy Projects Matters, in One Simple Chart,” Climate Progress, June 7, 2012: here

3 See the Nikkei BP English-language version of the September 27, 2010 release of their report at: here

4 The Fuji Keizai assessment also projects global smart community projects to increase from ¥16.332 trillion in 2011 to ¥40.555 trillion by 2020

5 On this see, “Rebuilding Eco “Future Cities” in Tohoku”: here

6 See (in Japanese) “Tokyo’s Power Generation Plan is Aimed at “Blowing a Hole” In Tepco,” in Zakzak, July 3, 2012: ZakZak here

7 Figures compiled by author, from local and national budgets.

8 For example, in his “Not enough land for solar,” in the November 2012 edition of The Oriental Economist, the very astute student of Japanese power markets, Paul Scalise, expresses concern about the “need for government subsidies in the form of a feed-in tariff” (p 11).

9 An excellent summary discussion of Japan’s feed-in tariff and charts of the price schedules and other features can be found at Eric Johnston, “A Guide to Japan’s New Feed-in Tariff,” Fresh Currents, August 23, 2012: here

10 For a succinct explanation of these items, see Eric Johnston, “New feed-in tariff system a rush to get renewables in play,” Japan Times, May 29, 2012: here

11 On this, see “Germany – 26% of Electricity from Renewable Energy in 1st Half of 2012”: here

12 On this, see the very cogent analysis by Gerard Wynn, “German power generation moving against utilities,” Reuters, November 27, 2012: here

13 Among the evidence is the accelerating pace of ice melt. See Joe Romm, “Science Stunner: Greenland Ice Melt Up Nearly Five-Fold Since Mid-1990s, Antarctica’s Ice Loss Up 50% in Past Decade,” Climate Progress, November 30, 2012: here

14 An example of the debate is seen in Phil Carson, “Utilities and us: towards an energy ‘ecosystem,’” Intelligent Utility, November 8, 2012: here

15 On this, see “US Department of Defense & Renewable Energy: An Industry Helping the Military Meet its Strategic Energy Objectives,” ACORE, January 2012: here

16 See Keith Johnson, “Navy Biofuel Plan Gets Senate Support,” Wall Street Journal, November 28, 2012: here

17 A concise summary of the approach can be found at Paul Krebs, “Department of Defense Makes Waves in the Renewable Energy Industry,” Energy Acuity Blog, October 3, 2012: here

18 On this, see “Are the Services Considering Nuclear Energy?” Defense Communities, August 9, 2012: here

19 The agency’s home page is: here

20 On this, see Andrew DeWit, “Japan, the Pentagon, and the Future of Renewable Energy: Battle Lines Form,” Japan Focus, March 4, 2012: here

21 A prominent example of the latter is IHS CERA, perhaps the premier association of conventional energy, as is evident from its website: here

22 The Agency announced on February of 2012 that it would produce an annual market forecast of renewable energy to complement its reports on conventional fuels. The IEA has long embodied a profound bias to conventional energy, yet even it has recognized that renewable energy “is now the fastest growing sector in the energy mix and accounts for almost one-fifth of all electricity produced worldwide.” See Erica Gies “International Energy Agency (Finally) Acknowledges Ascent of Renewable Energy,” February 28, Forbes: here

23 An amusing and very instructive account of the IEA and other agencies’ bias in energy projections can be found at David Roberts, “Why do ‘experts’ always lowball clean-energy projections?”, Grist, July 1, 2012: here

24 The Energy Watch Group’s roots and mission are described in its August 2010 publication, “Energy Policy Needs Objective Information, Objectivity Needs Independent Financing”: here

25 For example, see the summary of the Energy Watch Group’s January 2009 blistering critique of the IEA’s projections of wind power, in James Murray “IEA accused of ‘deliberately’ undermining global renewables industry,” Business Green, January 12, 2009: here

26 IRENA was largely inspired by the now-deceased German parliamentarian and energy expert Hermann Scheer. His comments on IRENA’s founding can be found at: here

27 After the flood of exuberant expectations that America would become a net oil exporter by 2017, more knowledgeable and critical observers have begun rendering detailed critiques. One of the best is Kjell Aleklett, “An Analysis of World Energy Outlook 2012,” Energy Bulletin, November 29, 2012: here. Among the items Aleklett highlights is the fact that the IEA’s 2004 outlook saw Saudi Arabia producing 22.5 million barrels of oil per day by 2025, but now projects a mere 10.8 million barrels per day by 2025.

28 Indeed, one of the principal organizers of the coalition of interests that helped push back opposition to biofuels was retired Marine Corps Lt General Richard C. Zilmer. Zilmer was the front-line commander in Iraq’s al Anbar province who in 2006 requested renewable energy and helped accelerate the green shift in the military. On this, see Geoffrey Ingersoll “The Strongest Argument for Renewable Energy Comes From the US Military,” Business Insider, September 25, 2012: here

29 The figure is from Herman K Trabish “The Water-Energy Nexus and Our Infrastructure Gap,” Green Tech Media, February 16, 2012: here

30 The figure is from Tascha Eichenseher “Clean Energy the Solution to Western US Water Woes,” National Geographic, July 26, 2010: here

31 On this, see Stockholm Environmental Institute, “New version of SEI’s water planning software links easily to energy tool for nexus analyses, adds IWMI environmental flow assessment module,” September 5, 2012: here

32 See, for example, (in Japanese) Mizutani Akio “Development towards International Standards Requires Policy Back-up,” Toyo Keizai, November 22, 2012, pp. 34-37. Some very good work is also available (in Japan) from Takahashi Hiroshi, Research Fellow at Fujitsu and a major figure in policy advice. See for example his English abstract: “Lessons on Smart Grids from Scandinavia,” Fujitsu Research No 366, February 2011: here

33 The chart is from Nicos Komninos “Global R&D 2011 Forecast,” URENIO, March 20, 20011: here

34 Hitachi’s home page on its power-unit options is nothing less than a paean to bigness.

35 On this, see Micheline Maynard “With Eye on Profits, G.M. Began Missing on Innovation,” New York Times, December 6, 2008, p.1.