Abstract

This article introduces the Japanese Furusato Nozei Tax System, whereby citizens can designate part of their tax burden to be transferred to as a financial contribution to a prefecture or municipality of their choice, thereby creating an alternative means of taxation. Given that the Furusato Nozei System is gaining widespread popularity, this paper investigates some of its inherent contradictions, its rationale, history and certain paradoxical features of this controversial tax system.

Keywords: Taxation, Paradox, Equality, Regions, Citizenship

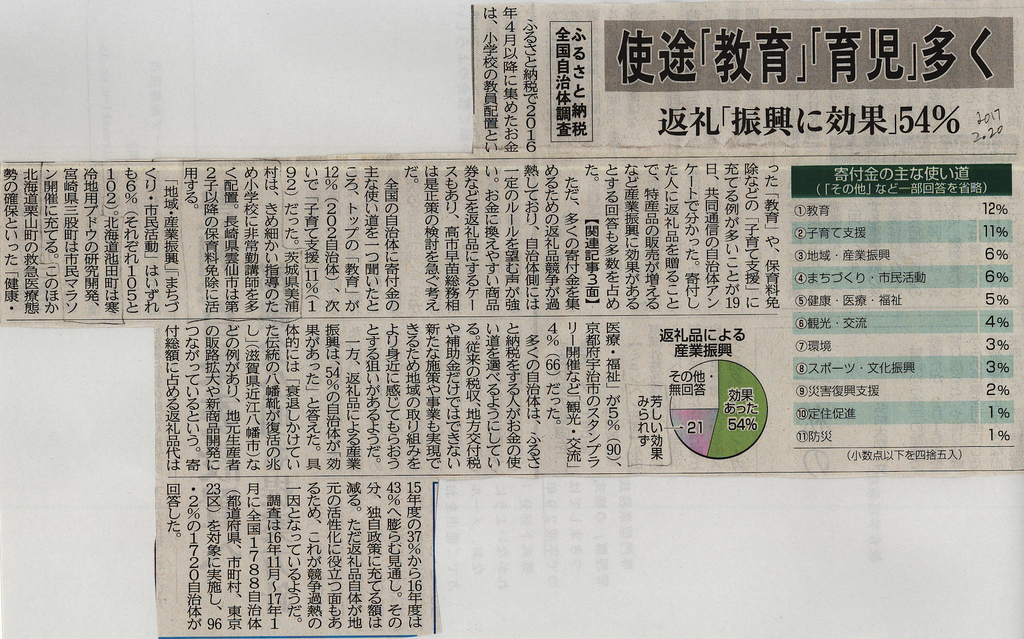

A front-page article in the February 20, 2017 morning edition of my local newspaper announced that the majority of the furusato nozei tax contributions that had been directed to prefectures and municipalities around Japan were to be allocated for education and childcare (see Figure 1). Originally envisioned as a way for individuals who had relocated from their hometowns to contribute financially to the economic health of their hometown, the furusato nozei tax system, a tax deducation/allocation system begun in 2008 whereby taxpayers from throughout Japan can direct their tax payments to the prefecture or municipality of their choice, seems to have become widely popular by 2016. This paper will examine the furusato nozei tax, illuminating its rationale, reality, controversies and implications. Part of any assessment of the system will rest on what one sees as the essential basis of a taxation system, whether that is fairness, response to social needs, or an orientation towards economic growth. Specific to the furusato nozei tax system as it stands now, questions can be asked as to the degree the system operates on the basis of personal consumption rather than shared citizenship, the implications of tax contributor influence on local policy, and whether the system prioritizes certain sectors of a local economy over others and puts local areas in competition with one another.

Furusato Nozei Tax, 2016: Designated Policies and Return Gifts

As detailed later in this paper, the 2016 furusato nozei tax data shows over 400,000 contributions for total tax deductions worth 22 billion yen and contributions worth over 24 billion yen. The article referred to above, carried in the Toonippo, the de facto Aomori prefectural newspaper, cited a fall 2016 Kyodo Tsushin survey of 1788 governing bodies from throughout Japan, including prefectures, municipalities and the 23 Tokyo wards. According to recent rule additions associated with the furusato nozei system, contributors, in addition to selecting a ‘place’ (prefecture or municipality) to which to direct part of their tax payments, can in some cases indicate policy areas to which they would like their contributions to be applied. According to the results of the Kyodo survey, and presumably at the request of contributors, 12 percent of such designated furusato nozei tax contributions nationally were to be allocated toward education, with 11 percent to be allocated to child support services. Six percent were to be allocated for two areas: regional and industrial recovery was one and town making and citizen activities the other. Health, medical and welfare services was to have garnered five percent, tourism and exchange activities four percent, and the local environment and sports/cultural activities three percent each.

|

Figure 1. Furusato Nozei Tax National Administrative Survey: Education and Childcare are Major Uses. Source: Toonippo, 20 February, 2017 |

The article also included selected examples of how the money was to be used within these policy categories. The article stated that a village in Ibaragi prefecture would put the revenue to use in securing adjunct instructors for elementary school education, while a city in Nagasaki would use the money to provide childcare costs for families with over two children. A town in Hokkaido indicated that the money would go to researching cold resistant grapes, with a town in Miyazaki indicating that the money would fund a citizen marathon. As for Aomori prefecture, the articles indicated that one-quarter was directed toward ‘town making’ activities (25%; see Figure 2), with 14 percent set for promotion of regional industries, eight percent for health, medical and welfare services, and another eight for tourism-exchange activities. For Aomori, only six percent was to be directed toward child support with three percent set to go to environmental-related policy programs. A 2017 Mainichi Shimbun article described how the Hakodate Municipal Government is using part of its 2016 ‘hometown tax payments,’ collected through 71 sources and amounting to 1.65 million yen, to cover the costs of a lawsuit opposing construction of the Oma Nuclear Power Plant, the location of which is shown below, set to be built in Aomori Prefecture, across the Tsugaru Strait.

|

|

The article quotes a government official as saying that the city would be pleased “if people develop an interest in this appeal of ‘stopping the construction of the Oma Nuclear Power Plant,’ through the hometown tax payment system” (Mainichi Shimbun, 2017).

As will be detailed below, most prefectures and municipalities now provide ‘return gifts,’ local goods (and sometimes services) to the individual furusato nozei tax contributor for their tax contributions. The Kyodo Tsushin survey found that over half (54%) of the locations saw provision of these gifts as a contribution to local recovery. However, 21% responded that no favorable effect could be seen, with the remaining quarter of respondents offering no response. According to a Saga prefectural city, selection of local products as gifts by the city has provided a boost to the weakening traditional crafts industries of the area, a highly beneficial local outcome of such ‘return gifts.’ Countering such positive aspects of the ‘return gifts,’ the article also points out that the portion of the contributions that are collected that go to provision of the gifts rose to 43 percent in 2016, up from 37 percent the previous year, meaning a decrease of the contribution that is applied to local policies. As for Aomori prefecture, responses regarding the effect of providing such return gifts on the local producers and general economy were split; 14 out of 39 responding municipalities indicated a positive effect, with 16 indicating no notable effect.

As indicated on a Furusato Nozei Tax System website, it is these two aspects—choosing where one’s taxes will be used and being able to receive a gift—that are the defining characteristics of the system and, as will be pointed out herein, the most alluring motivating factors (see Figure 3).

|

Figure 2. 25% to be used for ‘Town Making Activities’ Source: Toonippo, 20 February, 2017 |

Figure 3. “What is the Furusato Nozei Tax?” depicts the sad face of taxpayers with no furusato option and the happy times that the new tax system makes possible Source: Furusato Nozei Site |

Before focusing specifically on the furusato nozei tax system, a general understanding of the Japanese national, prefectural and municipal tax system is important. As outlined on a Tokyo Metropolitan Government website (n.d.), Japan has a three-tiered administrative-fiscal structure centered on the national government, but predominantly enacted at the lower two levels, the prefectures and municipalities. Thus, with the exception of foreign relations and national defense, much of the administrative functions of government are financed by combinations of national and local government budgets, with the policies and programs carried out by local governments. The website indicates that for fiscal year 2013 total national taxes collected from citizens amounted to 51.2 trillion yen, with local taxes collected at the prefectural level amounting to 16.8 trillion yen, and local taxes collected at the municipal level amounting to 18.6 trillion yen (see Figure 4). However, money from the national government was transferred, per existing law, to the prefectures and municipalities via Local Allocation Taxes, Local Transfer Taxes and Special Local Grants. Local Allocation Taxes (LAT), designed to ensure general revenue sources to prefectures and municipalities and to correct fiscal imbalances among local governments, thereby ensuring that local governments across Japan are able to provide an adequate level of services to local residents, form the core of the financial adjustment system at the local level for the nation. The Local Transfer Taxes (LTT) are based on a fixed proportional system based in gasoline, tonnage, automobile and special local corporate transfer taxes. For fiscal 2013, LAT transfers to prefectures and municipalities amounted to 17.6 trillion yen, LTT transfers amounted to 2.5 trillion yen, and special local grants to 125 billion yen. This means that the tax base is provided by approximately 60 percent in national level taxes versus 40 percent in local taxes, with allocations to national administrative services accounting for approximately 36 percent of this versus 64 percent to local governments. Thus, whereas a slight majority of the tax base is a national function, expenditures by local governments account for approximately 1.4 times those of the national government.An individual income tax, originally based on a progressive five-rate tax schedule, was introduced in Japan in 1887. Even early on, adjustments and additions were made: interest on bonds began to be taxed separately as of 1899, with interest on fixed-term deposits becoming subject to taxation in 1920. Fast forward through the war years and, American occupation the tax system came to be based on an American-type system, being comprehensive and generally progressive. But as the Japanese economy grew through the 1960s and ‘70s, the broad tax base gradually eroded. The ‘fundamental tax reform’ of 1986-88 attempted to recover the comprehensiveness of the system by eliminating or reforming many of the provisions that had weakened the depth and breadth of the tax base. At present, taxes in Japan are paid on national, prefectural and municipal levels on income, property and consumption, as well as vehicle-related taxes and taxes on liquor, tobacco and gasoline. While asserting that the disparity of income and wealth is one of the most important and serious problems in Japan, Kaneko (2009) noted that reforms undertaken in the mid-2000s changed the taxation schedules for financial asset-derived income, meaning the Japanese system is now labeled a semi-dual income tax system. Most recently, the Liberal Democratic Party and the Komeito announced a tax plan that has been labeled by some as a first step toward raising the base level of Japan’s growth potential, by incorporating flexibility in allowing for corporate reorganization in response to global competition, while others have expressed disappointment in the deferral of elimination of spousal deductions, a means of promoting women’s participation in the workforce (Shigeki, 2017).

Japanese Income Taxes and the Furusato Nozei Tax

|

Figure 4. Structure of Local Finance in Japan Source: Tokyo Metropolitan Government website FY2013; unit: yen 100 million. Furusato Nozei Tax |

As explained on the Ministry of Internal Affairs and Communication Furusato Nozei Portal Site (Ministry of Internal Affairs and Communication, n.d. a), the furusato nozei tax is a system whereby a portion of the taxes owed by an individual can be voluntarily contributed to a specific regional governing body, a prefecture, municipality or special district, yielding a decrease in overall tax burden according to a set schedule. The specific provisions of the furusato nozei tax are set out in Section 37 of the Regional Tax Law and were promulgated in spring of 2008. The specifics of the law allow that an individual can reduce taxes owed by set percentages by making a contribution at the appropriate level. Offered as an example of the system at work on the Furusato Nozei Site (TRUST BANK, n.d. a.), if a contribution of 40,000 yen is designated as a contribution to a prefecture or municipality of the individual’s choice based on the furusato nozei system, 38,000 yen of tax burden will be deducted from the contributor’s regular tax burden.

Debate, both political and public, regarding such an addition to the tax system began with a 2006 March opinion piece in the Nihon Keizai Shimbun, which proposed a Regional Improvement Furusato Tax System. The governor of Fukui prefecture at the time stated that such a tax system would work to reduce the finance and service gaps between regions and contribute to the slowing of depopulation of rural areas by providing for program funding for areas experiencing such trends. Over the period of debate and to the present, the merits and demerits have been clearly identified by supporters and detractors.

As for merits, furusato nozei tax funds are seen as vital for areas where economic growth, if not long term economic stability, is inherently difficult. Contributions directed to specific prefectures or municipalities are seen as representing either investments in the future of such places or re-investments on lost opportunity. Regardless of whether the money is designated for a specific policy area or not, such contributions increasingly provide a notable component of larger prefectural and municipal budget planning. Taking the case of education, rural areas often face an investment loss in this area, as many young people who have been educated by their regional cities, towns and villages, relocate to larger urban centers for employment when they become adults and never return to their hometowns. Nevertheless, prefectures and municipalities are charged with providing public education to local youth. Thus, a contribution directed to a prefecture or municipality to be allocated for education can be framed either as a re-investment in a local area directed specially to cover such lost education expenses or as a shared provision of future education costs (partially by areas where the youth will relocate and partially by the rural municipality itself). Another area where the furusato nozei tax system is now starting to show some effect is in providing a stable planning environment in specific budget areas, for example, in the ensured continuation of local area traditional crafts used as gifts for contributors.

The demerits that have been identified refer, first of all, to the fact that some areas are simply less attractive and garner less attachment, and subsequently fewer contributions, than other areas, thereby creating a negative imbalance between areas that can attract additional revenues and those that cannot. A second demerit comes with the complications of government planning and service provisions that accompany furusato nozei tax payments. The central government, along with prefectural and municipal governments, must administer such tax transfers, creating additional workloads. An additional complication is in budget planning: as local municipal governments cannot accurately predict the outcome of furusato nozei tax transfers, whether a loss as locals contribute taxes elsewhere or a gain as contributions come in from contributors in other parts of Japan, near and long term planning becomes increasingly complicated. In cases where local residents may have contributed tax payments elsewhere, but few contribution emerge from other areas, the municipality may face a significant burden to replace the lost revenue. Further, as costs of providing local services varies from region to region, the flow of revenue from areas of high service provision cost to an area of low service cost (or vice versa) based solely on such sentiments as affection creates a service imbalance nationally. While in some cases, such flows of tax revenues may lessen regional gaps, in other cases the gaps inevitably increase, meaning as critics contend, the furusato nozei tax system is neither an equitable nor predictable policy to address regional imbalance over a national scale.

Although relatively simple in origin, a visit to the Furusato Nozei website (https://www.furusato-tax.jp) reveals how complex the system has become. At the top of every page, six ‘choices’ are offered, which direct the user to specific ‘contribution’ category pages: a ‘gift choice’ page, a ‘region choice’ page, a ‘use choice’ page, a ‘ranking choice’ page, a ‘recommendation choice’ page and a ‘disaster support’ choice page. As shown in Table 1, the ‘gift choice’ page presents 22 categories, each with what can only be described as an overwhelming number of choices.

|

Table 1. Gift Choice Options by Item Area, Nationwide Source: Furusato Nozei Site |

As can be expected, the ‘regional choice’ page is divided up by region and prefecture, after which each municipality either provides information on the page or requests application for further information and options. Parsing out options at the prefectural level would be, similar to the overwhelming number of choices for ‘gifts’ as indicated above, confusing if not impossible. Taking the case for a smaller area, Hirosaki, one of the three large cities of Aomori Prefecture (but not the prefectural capital nor site of a Shinkansen station), boasts 99 items at four support levels. Ignoring double counts on items in multiple categories (Hirosaki is at the center of the Tsugaru apple-growing area, thus many items feature apples in one form or another; for the local lacquerware, found in such forms as chopsticks, cups, bowls, pens and serving platters and tea sets), there are 36 items available at the 10,000 yen support level, 24 items at the 20,000 yen support level, 20 items at the 30,000 yen support level and 19 items at the 50,000 yen support level. The ‘use choice’ page lists 18 policy areas: nature preservation, tradition preservation, public space works, medical-welfare, music, international exchange, the aged, NPO-association support, festival activity, tourism, environment-scenery, children-youth, culture-education-lifelong learning, agriculture-fisheries-industry, sports, disaster recovery, other, and ‘leave it to us (omakase)’. The ‘disaster support’ page lists ‘recent’ projects in twelve areas including seven related to earthquakes, four to typhoons and one to the Itoigawa Fire that occurred in 2016. As of April 2017, the running total provided for ‘disaster support’ contributions was 2.567 billion yen. The page also indicates that there were 8,022 contributions for a value of just over 231 million yen allocated for the Itoigawa Fire, which destroyed over 150 buildings in a Niigata city.

Furusato Nozei Tax: By the Numbers

The year-by-year increase in furusato nozei tax contributions is shown in Table 2. As shown, the number of ‘applicants,’ which is to say contributors, along with contributed and deducted amounts were stable with little variation, at 33,000 contributors and 6.5 to 7.2 million yen, until 2012 (tax year 2011). As will be further detailed below, the massive increase, followed by a subsequent decrease (but to levels higher than before) represent contributions directed to the victims of the Great East Japan Disaster of 2011. Also notable is the increase from 2015, attributable to changes in the rules allowing higher deductions and more aggressive marketing for the program.

|

*1 tax year 2008; same for every year *2 as of June, 2016 Table 2. Furusato Nozei Trends Source: Ministry of Internal Affairs and Communication, 2016 data |

As provided in a Furusato Nozei Archive (Ministry of Internal Affairs and Communication, n.d. b), one can discern participation trends at the prefectural level nationally and within any prefecture and regarding whether the contribution reflects a loss to the prefecture or to the municipalities within the prefecture. As can be expected, the two largest locations in terms of participants are Tokyo and Osaka, accounting for from one-quarter to 30 percent of contributions. Nationally, the contributions made elsewhere versus the revenues deducted by prefectures have ranged from 26 percent for 2008 (7.26 billion yen contributed externally versus 1.89 billion yen deducted from revenue base) to 54 percent for 2014 (34 billion yen contributed versus 18 billion yen deducted). Prefectural averages for each year (2009 to 2014) reflect a similar range of variation. In the case of the latter trend, across both the seven years of data and the geographical breadth of Japan, the balance between tax revenue losses to prefecture versus municipalities is 40 percent for the prefecture and 60 percent for the municipalities, meaning that municipalities are suffering revenue losses at a higher rate than prefectures.

Looking at the 2015 furusato nozei tax system results (Ministry of Internal Affairs and Communication, n.d. c), opinions regarding the reasons for these increases, as described from the recipient side (the prefectures and municipalities) were indicated as the attractiveness of the gifts (41%), the ease of making a contribution (16%), the ‘popularization’ of the furusato nozei tax system (15%) and the effect of effective program promotion (13%). The 2015 report also includes recipient level data from 2008 by prefecture, the pattern for which is quite interesting. In 2008, the first year, the amount received by Tokyo was the highest of any prefecture, at 1.4 billion yen, while the number of contributions to a site was highest for Hokkaido, at 5,222. However, by 2015, Yamagata surpassed both Tokyo and Hokkaido, with 5.05 billion yen in receipts and 289,258 contributions to its finances, topping Hokkaido’s 4.28 billion yen and 268,950 contributions. Indeed, in terms of revenue received, Tokyo in 2015 ranked 12th and by cases, third from lowest.

An additional telling aspect of the furusato nozei tax system that is apparent in this data is its potential to allow residents throughout Japan to respond to events, in the case that follows, a natural disaster. While the receipts and cases for outlying Japan were strikingly lower than for Tokyo, and to a lesser degree Osaka (the exception being Hokkaido, as above) from 2008 to 2010, this all changed in 2011. In response to the 2011 disaster, the receipts and cases for Iwate Prefecture, where coastal areas were hard hit by the tsunami associated with the 3.11 earthquake, shot up from 178 million yen and 899 cases in 2010 to 2.87 billion yen and 9,463 cases. In other words, the amount of furusato nozei tax revenue directed to Iwate rose by 16 times from 2010 to 2011, with the number of contributions rising by ten times. The jump is similar for Fukushima Prefecture, also hard hit by the disaster, but in addition hampered by fears of radiation-based food contamination in its domestic food sales market, where the 2010 revenue of 132 million yen jumped eight times to 1.138 billion yen and the cases seven-fold from 1,094 to 7,301.

Taxation and Redistribution:

Fairness, Needs or Growth; Direct and Individual versus Indirect and Regional?

The controversies and implications associated with the furusato nozei tax system are now becoming apparent. However, in order to more clearly illuminate these, one must step back from the furusato nozei tax system itself and consider the fundamental realities and debates regarding taxation and redistribution.

Governments at all levels need to raise revenue in order to finance public-sector expenditures; taxation is the price we pay for government services. Governments thus set up tax systems to collect revenue from a variety of sources and through a variety of means—citizens included. These taxes include income tax, enterprise tax, property tax, consumption tax, vehicle-related taxes and liquor, tobacco and gasoline taxes. Distribution (or redistribution, if one prefers) of taxes, in terms of amounts, policy areas, and the manner of distribution represents the other side of the tax coin, where the major debate is the degree and manner to which a society attempts to (or not) decrease income and social inequalities or push certain policy agendas. While tax policy is first and foremost situated within the realm of econometrics, Prasad (2008) pointed out that tax redistribution is a matter that is primarily political, in which the competing voices of democracy reflect competing claims for fairness, need or growth. In this, tax redistribution reflects either a prioritization of efficiency through equity provision so as to promote economic growth or the pursuit of social justice as either an ethical imperative or to provide for a stable society. Operationally, tax redistribution can be achieved either through broadly social and generally indirect funding transfers, such as funding for education, health and other social services, or through direct and sometimes specifically individual monetary transfers, such as social assistance benefits and social insurance programs. And while there are controversies over the appropriate levels of taxation for various economic and social citizen profiles (rich versus poor, investor versus worker), the specific topical segmenting (corporate, income, consumption, residential) and manner and focus of the distribution of collected taxes for those public-sector expenditures, most view paying taxes as a form of citizenship. In this system, the citizen supports the nation through payment of taxes, with the government determining both appropriate taxation levels and appropriate distribution of these taxes based on policy priorities that emerge out of the democratic process of voting and elections (Figure 5).

|

Figure 5. A Citizenship View of Taxes |

While the Meltzer and Richard (1981) ‘rational choice’ model has long been the anchor for any consideration of the politics of tax redistribution, the ambiguity of its empirical evidence and questions about its plausibility have generated other views. Advances in experimental economics have pointed out that subjects often employ strategies and exhibit behavior that does not necessarily maximize an expected payoff, the basis of most economics-based models, which indicates that notions of fairness and need do affect economic decisions and behavior. Alternative models of taxation have been advanced that reflect political sociological views (Goodrich, n.d.), that incorporate both income redistribution as well as public good provision (Ihori & Yang, 2008), and that are cognizant of inequality, even regional inequality (Kessing, Lipative & Zoubek, 2015). In terms of the social psychology of redistribution, Ohtake and Tomioka (2004) found that although income level is generally negatively correlated with support for redistribution (higher income generally yields less support for high redistribution), dynamics such as expectation of future unemployment do tend to affect levels of support. They point out that while altruism can be a key factor, the character of such altruism may be either recipient-oriented, at an individual level where the benefit goes directly to the recipient, or contributor-oriented and at a broader societal level, as when support for higher levels of taxation is based in concern regarding negative externalities such as widespread social unrest that may result from social inequality. In this sense, a rise in income inequality at a societal level generally has a positive impact on approval of redistribution, which acts to stabilize society. However, Alesina and Angeletos (2005) also point to social beliefs that see ‘fairness of social competition’ as the basis of tax redistribution. If societal equilibrium and steady state are desired (as we should generally assume), it is likely that a society that believes birth, connections, corruption and luck determine wealth will levy high taxes that trend toward redistribution, with an aim toward increased social stability in the face of systemic inequalities. However, a society with ample and equal opportunities and social mobility where many believe that the equilibrium and stability of society emerge with success gained through individual effort and that all have a right to enjoy the result of their individual efforts will, conversely, likely lean toward low taxes and low redistribution. In this sense, fairness, needs and growth are equally valid underlying notions for taxation and redistribution in various societies, and the trends, whether toward higher taxation and higher redistribution or lower taxation and less redistribution, can be quite variable over time and place and from individual to individual.

That said, notions of equality are core to Wilkinson and Pickett’s (2009) The Spirit Level, which popularized the ‘income inequality hypothesis’ holding that more equal societies have superior health and social well-being: a society with low income inequality will tend to exhibit higher social well-being than a society with high income inequality. Research by Ballas, Dorling, Nakaya, Tunstall and Hanaoka (2013) found support for this by empirically testing the income distribution and social mobility of the UK and Japan. They found that Japan remains a relatively stable and equal country with low levels of inequality, which may psycho-socially influence people’s trust, compassion, optimism, as well as their lives and health. In this sense, high taxation and redistribution would likely be accepted as both a pre-condition for and a reflection of social equilibrium and stability.

***More recently, Tay (2015) pointed toward two additional compelling factors regarding attitudes toward tax redistribution: subjective income inequality and spatial locality objective income. The research found that regardless of levels and patterns of objective income inequality, an individual’s level of tolerance for subjective income inequality is a robust predictor of preference for redistribution. However, the research also found that spatial locality objective income—a region’s objective income inequality—does not systematically influence individual preference for redistribution: whether an individual lives in metropolitan Tokyo or the outlying agricultural areas of northern Japan, the levels of objective income inequality between the regions do not systematically affect a person’s redistributive preferences. Tay’s findings support the idea that subjective income inequality (rather than any quantifiable place-dictated indicator), through individual tolerance of inequality (rather than a social status indicator), has significant influence on support for redistribution.

In summary, the fundamental controversies of taxation, and in particular redistribution, relate to which of three notions a society prioritizes—societal fairness, resolution of needs or fiscal growth—and whether such objectives are to be met through redistribution that is direct and at an individual level or rather indirect and distributed more broadly at a societal level or through a regional mechanism. Specific to the case of the spatial inequalities in contemporary Japan, in the citizenship view of taxes outlined above, citizens of rural areas would expect that the central government will address their needs through fair redistribution of collected taxes in a manner where the generated opportunities for growth are balanced geographically across the country rather than with the usual focus on larger urban and industrial areas. In this sense, the citizenship model acquiesces policy priorities to the government, but implies that citizen expect that their situations and needs will be taken into account in a manner that is fair and will contribute to societal stability and growth. The furusato nozei tax system, however, adds an additional element to this citizenship model: the option for any individual to subvert the policy priorities of the government, both central and local, and direct their taxes to focus on a specific place or place and policy.

The Furusato Nozei Tax System: Shared Citizenship, Personal Consumption or Rural Competition?

In a collection of papers from the Japanese Studies Association of Canada 2015 conference on the theme of “Culture, Identity and Citizenship,” Rausch (2015) argued that one area where a sense of shared sacrifice for shared investment resulting in regional vitalization in rural Japan could be realized was in the furusato nozei tax system. The assertion of the paper reflected an orientation that Japan, both as a nation governed at large and as a nation of individuals acting as Japanese citizens, was called upon to share the sacrifice of investment in regional revitalization. This would be realized through the distribution and allocation of public-sector expenditures by the central government toward places and policies that were deemed to need them and by individuals through their furusato nozei tax contributions toward those specific places that these individuals were concerned about or interested in. This represents an expanded notion of the Citizenship View of Taxes shown in Figure 5.

Summarizing from that paper: Whereas citizenship historically focused on the civic, political and social rights of citizens . . . citizens today are largely passive participants of citizenship, convinced that conspicuous consumption, payment of (minimal) taxes and occasional voting are the only citizenship acts required of them. Other notions of citizenship have, however, been articulated: cultural citizenship, which stresses the centrality of culture and identity for an understanding of citizenship, where the challenge of conception and practice is to bring identity as a cultural element into the consciousness and action of citizenship. Transformed into operational terms, the agency of such citizenship manifests itself through common experiences, processes and expectations, together with discourses and actions of empowerment that result in a triadic conception of ‘cultural-identity citizenship.’ (Rausch, 2015, 56-57)

While such a notion of citizenship can be realized through citizens’ simply paying their share of taxes and accepting governmental determinations of the best balance of distribution in terms of fairness, needs and growth, in terms of the current theme, this agency is articulated at an individual level through the furusato nozei tax system in the form of a revenue contribution to a geographically specific and sometimes a specific policy area (Figure 6). This is the expression of shared citizenship at the individual level, in the cultural-identity of shared investment for regional revitalization made possible through furusato nozei contributions.

|

Figure 6. A Shared Citizenship View of Furusato Nozei Taxes |

In this view, paying taxes as a contribution to a specific area and with a policy focus yields a good outcome for both taxpayer as contributor and local area as tax revenue recipient. The contributor gets to ‘feel good’ about a contribution to an location and policy of their choice through sense of cultural-identity citizenship and the location realizes a revenue boost based on this act of citizenship. Such notions of citizenship can also be considered in the case of furusato nozei tax contributions that are directed to disaster areas for recovery support. Separating out those contributions that represent altruism based on convenience—i.e. those who otherwise would not have contributed to disaster recovery were it not for the convenience offered with the furusato nozei system—from true altruism—those who would have contributed regardless but found the furusato nozei system to be the most convenient way—will require more research, but considering the level of disaster support contributions for 2017 indicated herein, it could be that the furusato nozei system may well represent the sleeping giant of disaster giving.

|

Figure 7. “Top Choices Recommendation Ranking, January 2017” shows some of the most popular return gifts of 2017 for those who choose the furusato option. Source: Furusato Nozei Site |

Regarding the furusato nozei system as a way of equalizing the fiscal inequality that exists in Japan, research points out that this is indeed, part of the outcome of the system. As Yabe (2017) concluded, the furusato nozei tax system has, to some degree, contributed to rectifying the unbalanced situation whereby large Japanese municipalities and those that are seats of prefectural governments are solvent, while smaller cities, towns and villages are experiencing severe fiscal hardship. The mechanism by which this has happened by Yabe’s measurement is two-fold. Municipalities that have high ‘public finance indexes,’ indicative of appropriate and stable fiscal governance, have, for the most part contributed more (through contributor’s individual decisions to contribute) to the furusato nozei system than they have gained from it and thus are seeing a furusato nozei deficit while still maintaining a high index rating. Conversely, municipalities that have relatively lower ‘public finance indexes’ are seeing a furusato nozei gain, as more tax disbursements are incoming than outgoing, which should help address their budget woes. Thus, from a municipal management viewpoint, the furusato nozei tax system could be deemed a success, with areas of high population that can absorb fiscal outflow contributing to areas of low population that benefit from fiscal inflow.

A 2015 NHK Closeup Gendai broadcast (NHK Closeup Gendai, 2015), echoed a similar argument, albeit expanding it wherein both the locality and the contributor gain a benefit through the furusato nozei tax system, while accompanying it with admission of an unavoidable and inherently controversial element of the furusato nozei tax system. The article cites a planning division official for the Hokkaido town of Tokachi, who illustrates the power of furusato nozei tax receipts by explaining that the additional tax revenues make it seem as if the village had doubled its actual population and that the furusato nozei tax system has yielded clear and meaningful changes in residents’ lives, particularly in the area of childcare services. However, the official also allows that approximately half of the value of the contributed tax revenues are returned to contributors in the form of local beef-based items, “a reflection of the local custom to give back half of what you received,” confirming that the enthusiasm for the furusato nozei tax system is in part, if not largely driven by the gifts that are offered in return for contributions. In this, the article highlights an increasing dilemma inherent in the system, as contributions are not based solely on local needs, but rather contributor preferences for local products, and thus prefectures and municipalities must now ‘attract’ contributions using only their local resources.

The controversy relating to reality of local gifts that is now a significant part of the furusato nozei tax system is obvious when one looks at the 2017 Furusato Nozei Products Ranking (TRUSTBANK, n.d. b.). The site shows, along with the most popular regional items on the basis of a ‘page view’ rank, the top nine in 15 specific categories. The top items are: Saga pork, Kumamoto oysters, Shiga beef, a Tokyo Skytree lunch, Yamagata rice and Kochi vegetables, along with meat and seafoods from other regional areas (12 total listed; see Figure 7). Provided on the page are items from throughout Japan in a range of categories: meat, rice-bread, fruits, seafoods, fisheries products, vegetables, sake and drinks, cakes, processed foods, noodles, cooking condiments-ingredients, travel and event tickets, miscellaneous daily goods, beauty and fashion, and traditional crafts goods (see Table 1). As outlined above, there is controversy regarding the appropriate value of the gifts, measured in terms of percentage of the amount of contribution, as well as whether provision of such gifts has a beneficial effect on the area, whether in such basic sectors as agricultural or the fishing industry and processed foods industries or in terms of traditional crafts and unique local foods artisans. In any case, the inherent and inescapable reality is that some locales have more attractive ‘return gifts’ available than other areas, gifts that are more appealing to a wider and possibly more urban audience than other gifts, so as to entice more and higher level furusato nozei tax contributions in exchange.

The NHK Closeup Gendai article quotes Uno Shigeki, professor at the Institute of Sociology, Tokyo University, who attempts to bridge this gap. While stressing that furusato nozei tax contributions do contribute to regional revitalization, whether through funding essential societal policies such as education, childcare and health services or by energizing and stimulating development in local industries, Uno also outlines how such transfers allow for non-residents the feeling of being involved in the creation and re-creation of local areas through actions that might be seen as those of a local resident. The furusato nozei tax transfers that now are rewarded with local gift products could be conceived as a way for non-local residents to participate in the policy making of a local area, assuming they designate a policy area for their contribution, as well as the consumption of local products of a local area. As indicated in the opening section of this paper, somewhere around half of the furusato nozei tax transfers nationally come with policy preferences/stipulations by the contributor attached, indication of a policy consciousness on the part of the contributor. However, given the popularity rankings referred to above, it is clear that the popularity of the gifts offered by the recipient prefectures and municipalities does, without doubt, influence the place where contributions are directed to some degree. In Uno’s attempt to bridge the gap between area policy and personal consumption, this balance is defined, rather kindly, as the contributor becoming a part of that place’s history and ongoing story.

Viewed, however from a broader perspective and in terms of the prioritization of fairness, needs or growth in how a society views redistribution toward societal equilibrium, the mere presence of the return gift alters the fundamental premise of a tax system and its approach and mechanisms of redistribution and raises pragmatic policy questions as well as philosophical quandaries about the true intention of contributors’ citizenship. While the contribution, regardless of the specific motivation, does connect the contributor with the locale, as Uno asserts, the balance for the contributor between consideration of public policy directive versus the opportunity to make a gift selection is a vital dimension. As shown in Figure 8, the essence of the gift component of the furusato nozei tax system complicates the notion of shared citizenship, creating an individual reward view of the furusato nozei tax system.

|

Figure 8. An Individual-Reward View of Furusato Nozei Taxes |

In this case, while a citizen chooses both to pay more than taxes as an act of citizenship and in so doing gets to ‘share’ in the support of a specified area with a sense of shared citizenship, by the mere act of choosing a place, presumably and partially, if not fully, on the basis of and in exchange for an appealing gift provided by that area, creates a paradox of taxation.

Implications of the Furusato Nozei Tax System

There are two major implications that can be drawn from this consideration of the furusato nozei tax system and can highlight the philosophical complexity of such tax and tax redistribution reforms as well as inform us in consideration of the future acceptability, if not viability, of the system.

The first implication arises on the contributor side of the furusato nozei equation. The progression articulated in this paper was from the obligation of simply paying taxes giving way to notions of citizenship in paying those same taxes (Figure 5), followed by this one-dimensional notion of citizenship giving way to a sense of shared citizenship in supporting an area of one’s choice (Figure 6). However, when the return gift is included in this otherwise citizenship-based equation, there is the risk that the endpoint becomes an act motivated by self-interest in the form of gaining a return gift (Figure 8). Furthermore, designation of an area to receive the contribution is one part of this equation; the fact that the contributor can designate a policy area, meaning that determination of public policy through direction of revenue is thus taken away from presumably informed public officials and determined at an individual level, that of contributor, is worthy of attention. On one hand, one could question to what degree the non-local and possibly relatively uniformed furusato nozei tax contributor from some other part of Japan should have a say in the distribution of local taxes within a community, thereby influencing the otherwise informed directives by local government officials. On the other, democracy does call for, and presumably benefit from, the voice of its citizens; should there not be a mechanism for citizens to directly indicate where they would like their tax contributions to go? Ultimately, this final stage—the individual-reward view of furusato nozei taxes—brings a question of whether the system will come to reflect a vision of taxation and redistribution based on fairness, needs or growth as determined by informed officials or rather merely an expectation on the part of contributors that they can direct local policy through funding directive, all while choosing the place, whether on the basis of some true interest or just for sake of the return gift of his or her choice, similar to online shopping where the consumer procures a different local produce from a different area each year.

The second implication reflects the side of the area recipient—the beneficiary of the furusato nozei tax contribution and the source of the sought-after return gift. As above, the progression articulated in this paper revealed a transition from ‘taxes paid to a government that presumably redistributes those taxes fairly,’ to ‘taxes paid to area governments designated by citizens for policies chosen by citizens in exchange for gifts from those area governments.’ Given the inherent inequality of resources that local areas as recipient governments can draw upon to use as return gifts in order to entice contributions, such a system essentially replicates, if not reinforces a neoliberal winner-takes-all reality of rural place versus rural place that a shared citizenship approach to furusato nozei taxes was designed to address. The implications of such a tax system for the prefectures and municipalities are clear: identify, prioritize and publicize attractive return gifts. While in its origin, the furusato nozei tax system was based on capitalizing on individual’s connection, real or created, with a particular ‘place’ within Japan, insertion of the return gifts has undeniably altered that premise. Whereas the motivation for a furusato nozei tax contribution in the past could have been based on support of one’s hometown from afar, establishment or maintenance of some personal connection to a place (whether prior to or after making a trip, for example), or on the basis of an informed determination to help, primarily a specific place, secondarily through some policy prioritization, given the persuasive orientation of the TRUSTBANK Furusato Nozei website, it is clear that the focus is on the local product to be received.

For the prefecture or municipality, this creates a dilemma: promote and offer a particular good on the basis of its importance to the area based on tradition and culture or identify and designate a product that, while local, may play more on the sentiments of non-locals and the availability (if not price) of such goods in far-away cities. As shown above, the top items are food items, where the contribution to the local labor and wage economy may be minimal in the case of a minimally-processed item, and certainly not as labor intensive or temporally impacting as, for example, a traditional craft item. In a similar manner, use of the most popular local product as a gift item, while essential to attract contributions, ignores the totality of the area, where an economy built on a variety of industries would be better than a single commodity economy based on the local product deemed most attractive, partially if not fully on the basis of what can only be termed ‘free-market principles,’ by outsiders.

To close, the question of this paper concerns how we should view the furusato nozei tax system. Should it be viewed as an improvement on the traditional citizenship view of taxes? Indeed, many see the furusato nozei tax system precisely as a way for citizens to exercise judgment over their taxes, as a way to direct money to the places, and the programs, that citizens deem worthy, as means of empowerment to be used by Japanese citizens themselves in supporting the rural areas and the local products of their choice in their fight against fiscal disparity and economic decline. This view reflects a citizen who is informed, and concerned about Japan and the fate of the many places of Japan and the people of those places. This is the shared citizenship view of the furusato nozei tax system.

Alternatively, should the furusato nozei tax system be seen as a way for citizens throughout Japan seek to ‘buy’ desired local products—usually food products—through their tax contributions? In this way are they merely furthering the present status-quo of regional inequality by rewarding areas blessed with appealing ‘gifts’ in their quest to attract additional revenues? And does this undercut either an equality-based or needs-based tax redistribution system based on an empirical and rationalized system of governance and yielding an area versus area competitive battle of local products as the basis of a tax system?

The conclusion of this paper is that the furusato nozei tax system is all of the above; in other words, it is a paradox. It is, on the one hand, a system that allows citizens to choose the place for where and policy to which their taxes will be applied, albeit largely on the basis of personal consumption choices. And it is, on the other, a system that reinforces, but also rewards local originality in local product development and public relations skill in local products promotion, both of which ultimately provide positive outcomes for the ‘places’ and the ‘people’ of Japan.

References

Alesina, A. & Angeletos, G.M. (n.d.) Fairness and Redistribution, American Economic Review 95(4), 960-980, on-line document, scholar.harvard.edu/alesina/files/fairness_and_redistribution.pdf.

Ballas, D., Dorling, D., Nakaya, T., Tunstall, H. & Hanaoka, K. (2013) Income Inequalities in Japan and the UK: A Comparative Study of Two Island Economies, Social Policy and Society, on-line document, http://journals.cambridge.org/abstract_S1474746413000043.

Goodrich, B. (n.d.) ‘A Non-Meltzer-Richard Model of Redistribution’, on-line document.

NHK Closeup Gendai (2015) print version: here.

Ihori, T. & Yang, C.C. (2008) Tax Competition, Public Good Provision, and Income Redistribution, Asia-Pacific Journal of Accounting & Economics, 15, 277-290.

Kaneko, H. (2009) The Japanese Income Tax System and the Disparity of Income and wealth Among People in Japan. Proceedings from the 2009 Sho Sato Conference on Tax Law.

Kessing, S. G., Lipatov, V. & Zoubek, J. M. (2015) ‘Optimal Taxation under Regional Inequality’, on-line document.

Mainichi Shimbun. (2017) Hometown tax used to cover costs of anti-nuclear plant lawsuit, April 12, 2017.

Meltzer, A. H. & Richard, S. F. (1981) A Rational Theory on the Size of Government, The Journal of Political Economy, 89(5); 914-927.

Ministry of Internal Affairs and Communication (n.d. a) Furusato Nozei Portal Site, here.

Ministry of Internal Affairs and Communication (n.d. b), here.

Ministry of Internal Affairs and Communication (n. d. c), here.

Ohtake, F. & Tomioka, J. (2004) Who Supports Redistribution? The Japan Economics Review, 55(4), on-line document.

Prasad, N. (2008) Policies for Redistribution: The Use of Taxes and Social Transfers, Discussion Paper Series 194, International Institute for Labour Studies.

Rausch, A. (2015) Regional Revitalization as Culture, Identity and Citizenship: Promise, Peril and Shared Sacrifice for Shared Investment, Japanese Studies Association of Canada (2015) Conference Proceedings “Culture, Identity and Citizenship”; 55-67

Shigeki, M. (2017) A Mixed Grade for Japan’s New Tax Reform Plan, on-line document, http://www.nippon.com/en/simpleview/?post_id=3334.

Tay, S. (2015) Who Supports Distribution? Subjective Income Inequality in Japan and China, Economic and Political Studies, on-line document, http://blog.chinadaily.com.cn/blog-1040969-30230.html.

Tokyo Metropolitan Government (n.d.) Tokyo’s Financial System: Financial Structure of Local Governments in Japan.

TRUSTBANK (n.d. a) Furusato Choice, here.

TRUSTBANK (n.d. b) Furusato Nozei Products Ranking page site, here.

Wilkinson, R. and Pickett. K. (2009) The Spirit Level: Why Equality is Better for Everyone, London: Allen Lane.

Yabe, T. (2017) ‘Furusato Nozei’ ha Tokyo ikkyoku shuchu wo zesei, chiho wo kasseika shiteirunoka? Todofuken-shichoson shushi deeta to zaiseryoku tono kankei kara kangaeru, proceedings of the Chiiki Shakai Gakkai 42nd Conference.

Related article

Andrew DeWit and Elliot Brownlee, Revisiting Postwar Taxation in Japan and its Contemporary Implications, The Asia Pacific Journal: Japan Focus, Vol 8, Issue 39. No.2, September 27, 2010