Yu Zhou

Can Chinese companies innovate in cutting-edge technology? It is a question many have been asking in the last few years as the size and dynamism of China’s economy become apparent. This article focuses on the development of Chinese companies in the information and telecommunication sectors of industry, conventionally known as “Information Communication Technology” (ICT) [2], among the most dynamic, profitable and globalized industries.

It is often argued that China’s rapid economic growth and national competitiveness are driven by its booming export industry, powered primarily by foreign affiliated companies. In this way, China appears to closely follow the footstep of Japan, and other smaller Asian dragons, starting from labor-intensive industry and gradually moving up the value chain. This story is not wrong, but it is incomplete — two other factors are also at play in China: rapidly emerging competitive domestic firms, and a vast and dynamic domestic market. While the western business world is agog with enthusiasm about a Chinese market that it hopes to dominate, this study examines how this market, in conjunction with China’s export industry, are creating powerful synergetic forces for indigenous companies. I approach the rise of Chinese companies historically by retracing the footsteps of China’s most prominent science park — Zhongguancun (ZGC hereafter) in Beijing — where many of the most dynamic indigenous companies were born. The article concludes that the growth and competitiveness of China’s own technological companies may eventually create more lasting impact on the future global landscape than China’s vaunted labor force.

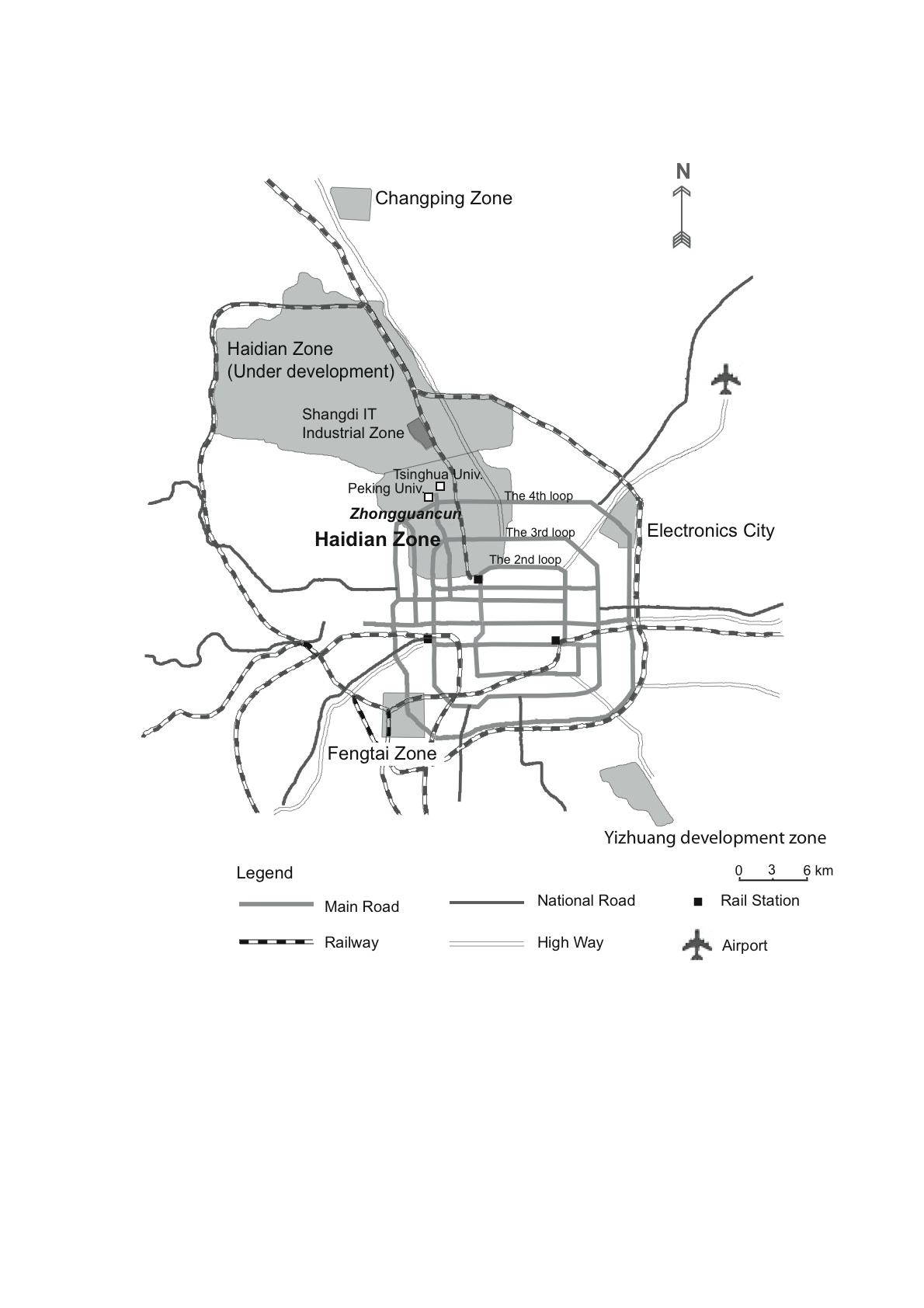

What is Zhongguancun?

Nestled in the northwest part of Beijing and home to many of China’s most prestigious universities and research institutes, ZGC is known as China’s “Silicon Valley.”

Since the mid-1980’s, ZGC has transformed from a quiet suburb designated for scientific research and higher education into a bustling hub of high-tech business and research and development (R & D) labs (Francis 1997). The following snapshots show the region’s startling transformation in a matter of years.

ZGC in the early 1980s. The peaceful are with wall-encircled universities or research institutes. Each institute formed a residential compound with few transactions outside. Haidian District archive.

ZGC in the mid-1980s. ZGC became known as the “Electronics Street”, with stores along the main thoroughfare selling computer hardware and software. Most were spin-offs from universities and the nearby Academy of Sciences. Haidian district archive.

ZGC in the late 1990s. Scattered office towers went up along the thoroughfare, and large indoor computer wholesale markets occupied the ground floors.

ZGC in the new millennium. The core of ZGC has become a corporate business center of high-tech Chinese and multinational corporations.

.jpg)

Figure 1: Growth of Zhongguancun Science Park (1988-2004). Source: Annual report of Zhongguncun Science Park, multiple years. (ä¸å…³æ‘科技å›åŒºç»æµŽå‘展综述, å„å¹´.)

ZGC is a different kind of technological region from the more familiar booming export-oriented hubs in China, exemplified by Shenzhen and Shanghai on the south and central coasts. Shenzhen and the surrounding area, Dongguan, developed since the 1980s as China’s first special economic zone, hosting China’s earliest and one of the largest clusters of information communication and technology (ICT) companies. Some of China’s most successful high-tech firms are located there such as Huawei; though the vast majority specializes in labor-intensive assembly for export. Shanghai and its environs such as city of Suzhou emerged in the 1990’s as a new center of high-tech production. It attracts more capital-intensive and higher-end manufacturing establishments, such as those making notebook computers and semi-conductors, than Shenzhen. Multinational companies from the United States, Europe, Japan and Taiwan play dominant roles in both Shenzhen and Shanghai. The majority of foreign investments there have targeted export markets, although in recent years investors have paid growing attention to China’s rapidly growing domestic market (Figure 2).

.jpg)

Compared to regions in other developing countries, ZGC also has unique features. Its enterprises did not grow out of a historically rooted business structure such as those in India, South Korea and Japan, where large, privately funded business powerhouses have long been in existence. All Chinese technological commercial firms had to be created — from scratch — in the post-reform era that began in the 1980’s. Further, ZGC does not feature multinational corporations (MNCs) as the dominant players, unlike in large Latin American countries such as Brazil (which also has a large domestic market), though MNCs have been welcomed as an integral part of the mix. And technological progress in ZGC has been driven primarily by domestic demand rather than export needs. Over 85 percent of ZGC’s revenue has come from domestic sales of products and services (Zhongguancun Administrative Committee 2005 p. 10). Many of China’s well-known ICT companies are found in ZGC: Lenovo, the world third largest person computer manufacturer; Baidu, China’s leading Internet search engine company; UFIDA, China’s largest privately owned software company; Founder, China’s largest digital media company; Datang, one of China’s largest telecommunication solution companies; Aigo, China’s leading portable storage and digital entertainment product maker, and Sina.com and Sohu.com, two of China’s most popular Internet portals. In other words, the advance of firms in ZGC is driven not by China’s most prominent advantage in the international division of labor — i.e., inexpensive labor — but by the ability to wed advanced technologies with the Chinese market.

Despite its prominence in China and pronounced global ambitions, ZGC remains an international enigma. Its origin in the centrally planned economy and its location in China’s capital invite skepticism over whether it will be able to compete with vibrant innovative centers in mature capitalist economies such as California’s Silicon Valley (Cao 2004). In essence, ZGC is an audacious experiment by a late industrialized country. China is not content with being simply a labor-intensive manufacturing workshop for foreign MNCs. Nor is it satisfied with technology acquisition and upgrading through a gradual process, through the export commodity chain, as some Southeast Asian countries have done. While that process is running its course in coastal China, China hopes that its enormous and fast-growing domestic market will also propel its best-endowed regions directly into the innovative technology market, while being open to MNC investment and competition. ZGC thus was designed as an incubator to create globally competitive technological leadership.

Thus far, ZGC has been relatively successful, though it is still far from reaching its ultimate goal. As one of China’s 53 national-level high-tech zones, ZGC generates about one-seventh of their total revenue (ZGC government website). About a quarter of the companies in the region derived more than half of their revenue from technology sales[4]. Of 25 Chinese technology companies listed on NASDAQ by 2005, 13 were located in ZGC. By 2007, about 100 companies in ZGC have been publicly listed in stock markets in China and abroad, easily a record among all China’s 52 national high-tech zones.

ZGC and Theories of Technological Development

If viewed through the most influential theories of East Asian technological progress, ZGC would appear to be an outlier. From Schumpeter onward, most theorists have held that technological changes constitute the driving force in the advancement of societies (M. Castells 1996; Malecki 1991; R. R. Nelson 1996). Yet how those changes occur under systems other than mature capitalism remains contentious. In the last three decades, the experiences of East Asia, particularly Japan, South Korea and Taiwan, have inspired two developmental theories.

The first holds that technological progress in newly industrialized countries is most likely to be achieved through a learning process consisting of borrowing, adapting, and improving upon foreign designs rather than through frontier innovation involving formalized R & D (Amsden 1989; Cumings 1987; M. Hobday 1995; M. Hobday 2001; Kim 1980). Export industries are thus the best catalyst and vehicle for technological learning, the theory argues, as external markets provide competitive incentives and require fiscal discipline of the producers.

The second theory maintains that the active engagement of states is indispensable in initiating and promoting industrial development and technological upgrades in developing countries. Skilled state interventions through timely subsidies, targeted industrial policies, capital investment, tax and regulatory incentives, and strict financial standards can speed up technology acquisition, this theory asserts (Amsden 1989; B. P. Evans 1995; Haggard 1990; Wade 1992).

The first theory tends to place least emphasis on the role of domestic markets in the technological trajectory of local enterprises in developing countries, as the previous regime of import-substitution was discredited as ineffective. If the domestic markets of the four Asian “dragons” are too small to merit much attention, the same cannot be said of the market of mainland China, one of the largest in the world (OECD 2006). The impact of such a market on domestic enterprises should not be underestimated.

China is also often said to support the theory that state intervention is essential for promoting technological development. But while the state has indeed played an indispensable role in developing ZGC’s technological programs and policies, it is only a part — and not necessarily the dominant part — of the regional quadrangular innovation system that has been taking shape since the 1980s in ZGC. That system consists of the state, MNCs, research institutions and local firms. Each should be understood as a reflexive actor in a transitional political economy facing the growing influence of globalization. The story of ZGC thus challenges the most influential wisdom on East Asian technological development by revealing how indigenous markets shape technological changes in a rapidly globalizing industry, and how institutional transformation takes place in technological sectors within a transitional economy.

.jpg)

The quadrangle system of innovation in Zhongguancun, Beijing.

Beyond the International Division of Labor

Since the 1980s, an enormous stream of literature has been produced based on a close examination of the development experiences of Latin America and East Asia. Consequently, a seismic shift has occurred in developmental theories. They now consider participation in the international division of labor as a prerequisite for development, while largely ignoring the roles of domestic markets and marginalizing the contribution of indigenous firms in such a market. Modernization theories in the 1960s and 1970s, in contrast, whatever their shortcomings, at least put more emphasis on domestic market development (Rostow 1971).

For developing countries, participating in the international division of labor means prizing export activities, starting from the bottom of the technological hierarchy with the hope of gradually moving up. Export industry is viewed as generating a path for technological acquisition. Stephan Haggard, for example, holds that the “crucial difference” between the East Asian and Latin American newly industrialized countries (NICs) is “the difference between industrialization through export and import substitution” (Haggard 1990 p.27). In a detailed comparative study of the “four dragons” — Taiwan, Hong Kong, Singapore and South Korea — Hobday (1995) presents a general model of technological learning through interaction with foreign firms. He emphasizes the importance of export, and in particular the Original Equipment Manufacturer (OEM) system [5] as a learning platform — “an enduring technological training school for later comers” (p. 192).

In contrast to the successes of East Asian export-oriented economies, the import-substitution policies adopted by large developing countries such as Brazil, India, and China between the 1950s and 1970s largely failed. Import substitution typically depends on prolonged protection of domestic industries, with high tariffs for imported goods. Protectionism leads to persistently weak performance by the firms in the international market. Scholars argue that import substitution also fails to reduce import dependency, achieve sufficient economic diversification, and alleviate social inequality in developing countries (P. Evans 1979; Haggard 1990; E. M. Porter 1990; Wade 1990). Based on these findings, the World Bank promotes export industries as a standard policy for economic development (World Bank 1993).

Yet, critics of export-oriented policies point out that export industry in many countries often amounts to labor-intensive assembly with little technological value (Dickens 1998). Not only do MNCs have little incentive to transfer core technology to developing nations, but even if they do the transfer often includes “know-how” (production engineering) but not “know-why” (basic design, research and development) (Lall 1984, p. 10; Dickens 1998; Porter, W. Philip and Sheppard, Eric S. 1998). These transfers therefore often reinforce the dependency of the receiving countries. Research on China’s trade and export sectors finds a profound dualism, with highly competitive industry in China dominated by imported technology and foreign affiliates. These firms are segregated from other domestic sectors and thus have a limited impact on local production and the diffusion of technology in China (Huchet 1997; Lemoine, Francoise and Deniz Unal-Kesenci 2004).

Even in the most successful export-oriented economies–upon closer examination—scholars have found that import-substitution has played critical roles during the take-off phases of several East Asian countries (Chang 2002, Webber and Ridgy 1996). Economic historian, Ha-Joon Chang (2002) portrays the new collective disregard of the domestic market strategies as “kicking away the ladder,” given that tariff and state subsidies for domestic industries have played crucial roles in the earlier development of western industrial powers. This suggests that the relationship between the dynamic of a domestic market and the development of domestic companies deserves more scrutiny. Export may only be one piece of a more complex puzzle of national technological capacity building.

China faces additional geopolitical limits to relying exclusively on export-based development. There are long-standing regulations banning U.S. firms from exporting certain potentially dual-use high technology to China. Due to its size, China is also susceptible to criticism of its successful export drive to the United States as a result of the large balance of trade gap. China therefore faces heavy pressures to open its own market to other countries, which Japan and South Korea were able to avoid from the 1960s to the 1980s.

Yet, large countries such as China have large and growing markets in their own right. OECD ranked China as the world’s sixth largest ICT market in 2005 (OECD 2006) and among the fastest growing. The Chinese home market thus allows domestic companies the opportunity to move directly into own-brand manufacturing rather than moving progressively from manufacturing others’ brands to creating their own. Indeed, quite a few Chinese companies developed their own brands only a few years after start-up, often without moving through the OEM phase. Yet, with many foreign companies competing to market their products in China, indigenous companies need to find ways to become competitive. This is no small challenge for under-capitalized and inexperienced indigenous companies facing MNC giants. Whether they can meet this challenge depends on their technical and managerial capacities. But an additional crucial factor is the presence of world-class export-processing facilities in China. With easy access to competitive, reliable, and high-quality component suppliers — the same suppliers for MNCs in the global industry — Chinese companies can target the Chinese market with special designs and pricing, given their intimate understanding of the market, as well as build their own distribution networks. If the market for their products also grows at this time, they have a good chance to best the foreign competition. Export challenges essentially reduced the learning curve for latecomers by helping them improve their technical competence and competitiveness, without requiring them to accumulate detailed engineering and processing skills in more complex components. As their design and marketing abilities improve, indigenous companies are able to progressively replace foreign products in the Chinese market, from the low to higher end. This process has created some of the fastest learners in the industry. Lenovo is among them.

Consequently, technological change in China may differ from that of other developing countries. The path of building Chinese companies’ competitiveness is best described as a synergetic model between import substitution and export upgrades. As shown in figure 9, China’s export industry and domestic market growth are two distinct processes driven by different global and domestic imperatives. When these two processes occur in the same or closely related sectors at the same time, one finds the most favorable conditions for technological learning and business competitiveness of China’s companies.

.jpg)

Synchronization of export upgrade and domestic market growth in China

Synchronization allows the entry and rapid rise of new manufacturers of mature technological products, as newcomers can tap into the existing global supply chain. The economies of scale enjoyed by the global parts suppliers together with the mass demand in China’s market enable the competitiveness in final products by Chinese companies. What’s more, intimate knowledge of the consumption preferences of a large domestic market may spur technical innovation and thus the development of products different from those in advanced markets. A high-quality export facility may help turn these innovative ideas into a viable commodity chain in a short time. Those Chinese companies that are able to locate the intersections of these two processes are in a stronger competitive position.

The synergy of the external and internal market may even foster a movement toward a more autonomous technological path than would otherwise be possible. Although China is not an advanced technological power, the Chinese state and Chinese firms have already started to develop technical standards that may have global significance. Thus far, technical standards have been the exclusive domain of the most powerful western or Japanese corporations and their counterparts in advanced countries. An export-oriented industry could only follow western technical standards to sell abroad. A closed import-substitution regime can impose domestic standards, but it is almost certain to be left out of the global mainstream. However, a combined import-substitution and export regime in a large market may create a more interdependent relationship between MNCs and local firms, making it possible to establish alternative standards. In short, the trajectory of China’s technological development needs to be understood not by treating export-oriented and domestic market-oriented activities as alternatives, but considering them as joint strategies for industrial development.

Institutional Evolution and the Role of the Chinese State

Studies of East Asia, and China in particular, tend to view the state as the paramount player in determining policy and political-economic outcomes. However, the relationship between technological development in ZGC and the Chinese state suggests a more complicated picture. ZGC is better characterized as a product of institutional evolution under globalization, in part tolerated and assisted but largely unanticipated by the state.

The role of the state and public policies in technological development, especially in East Asia, has been a subject of heated debate. Castells (1996) argues that the state plays a pivotal role: “If society does not determine technology, it can, mainly through the state, suffocate its development. Or alternatively, again mainly by state intervention, it can embark on an accelerated process of technological modernization able to change the fate of economies, military power and social well-being in a few years” (p. 7). Evans (1995) crafts a more refined model, situating the state in the institutional structure of societies. Depending on the degree of autonomy of states from different social interest groups, Evans divides states into two categories: predatory states, exemplified by Zaire, which extract resources with little service to citizens in return; and developmental states, like South Korea, which can formulate coherent and effective developmental programs and guide enterprises in technological development.

While emphasizing the embeddedness of the state in society, Evans clearly privileges the state in state-society relations. In contrast, institutional economists have long argued that institutions make the difference in economic performance. According to North (1990 p. 3): “Institutions are the rules of the game in a society or, more formally, are the humanly devised constraints that shape human interaction. In consequence, they structure incentives in human exchange, whether political, social, or economic. Institutional change shapes the way society evolves through time and hence is the key to understanding historical change.” North argues that institutional changes are overwhelmingly gradual and evolutionary. Through a search and selection process, the established “routines” which govern behavior at a particular time gradually give way to changes started at the margins (Malecki 1991; Nelson, Richard R. and Winter, Sidney G. 1982).

Institutional evolutionary theory sheds more light on ZGC than a state-centered approach does. Looking closely, the most prominent feature of the role of the state in China’s technological development is not its leadership but its high variability. In the People’s Republic, technological policies swung from defense-led projects to civilian sectors, from self-sufficiency to foreign dependency and then to autonomous innovation, from central planning to market driven, then to stressing state regulation and control. It is clear that it continues to search for a workable model for technological development.

The dramatic shifts in state policies over the last few decades, however, reveal a unique feature of the Chinese state compared to the states studied by Evans (1995): China’s central government is anything but stable in its policy framework. Ever since the reform and open-door policies beginning in the 1970s, new actors partially or largely beyond state control have been emerging, and the rules of the game are forever being contested and redefined. Actors are forced to adapt to an environment of heightened uncertainty. The development of ZGC illustrates this institutional instability. Rather than following a state issued blueprint of transformation, the region’s growth has been cyclical, evolutionary, and often chaotic and haphazard. The actors including state, MNCs, local firms and local research institutions are locked in a quadrangular innovation system in which each sees its influence wax and wane, and each is challenged by others and by the changing political and institutional environment (figure 8). New institutions have emerged, only to become inadequate a few years later. In short, like a reptile shedding its own skin, ZGC grows by generating and testing new identities, organizations, and strategies and by accumulating knowledge on technological management and innovation.

Far from being results of Chinese state policies, the institutional changes in ZGC are complex products of confrontations, bargaining, and conciliation among the actors in the regional quadrangular innovation system. The state’s actions and the effectiveness of its strategies are contingent upon their context. The same strategies that worked in one place at one time may not work in another place and time. Deng’s famous metaphor, “Cross the river by feeling the stones,” or Naughton and Segal’s “muddling through” (2003, p. 186) seem still to be the best ways to describe this untidy process.

Conclusion

What can we learn from ZGC’s experience about technological progress, not only in China but also in other developing countries? For one thing, we need to realize that indigenous companies are indispensable agents for cultivating and developing technology markets. Developing countries, in their pursuit of high technology, have a track record of attracting MNCs while paying little attention to their domestic companies. The story of ZGC shows that while MNCs can introduce advanced technology, they typically have standardized practices that are insensitive to local markets or inappropriate for them, especially when purchasing power is low. Left to their own devices, MNCs also lack the incentives, flexibility, and local knowledge to react to market changes. In contrast, indigenous firms understand their home court and have greater commitment and flexibility to bring appropriate and affordable technology to domestic consumers. However, MNCs, despite their drawbacks, are necessary partners for collaboration and potential role models to learn and perhaps importantly, deviate from.

Second, ZGC’s experience shows us that the roles of the state are necessarily multi-faceted. The state’s crucial jobs are not just providing specific policies or R & D capital but collaborating effectively with other technological agents and learning to reform regional institutions under changed circumstances. In other words, the state must be willing and able to adapt and respond to changes and demands by other agents. Institutional transformation has to be a learned process, as entrepreneurs, businesspeople, professionals, bureaucrats, scientists, and consumers learn to cooperate while the new rules of the game are being negotiated, established, and observed. In the long run, the technological trajectory of ZGC is neither magical, random, nor deliberately scripted. Rather, it is a dynamic adjustment process involving multiple actors negotiating through drastic and systematic shocks that often come at short intervals.

Yu Zhou is associate professor of Earth Science and Geography, Vassar College. She has published extensively on the Asian immigrants and their transnational business networks in New York and Los Angeles.

This article is a slightly revised version of a chapter in The Inside Story of China’s High-Tech Industry: Making Silicon Valley in Beijing.

Posted at Japan Focus on February 9, 2008.

Sources

Amsden, Alice. 1989. Asia’s Next Giant: South Korea and Late Industrialization. New York: Oxford University Press.

Cao, Cong. 2004. Zhongguancun and China’s high-tech parks in transition: “growing pains” or “premature senility”? Asian Survey 44, no. 5: 647-668.

Castells, Manuel. 1996. The rise of network society. Malden, MA: Blackwell Publishers.

Chang, H. Kicking away the ladder: Development Strategy in Historical Perspective. London: Anthem Press, 2002.

Cumings, Bruce. 1987. The origins and development of Northeast Asian political economies: industrial sectors, product cycles, and political consequences. In The Political Economy of the New Asian Industrialism, edited by Frederic C. Deyo. Ithaca: Cornell University Press.

Dickens, Peter. 1998. Global shift: the Internationalization of Economic Activity. New York: Guilford Press.

Evans, B. P. 1995. Embedded Autonomy: State and Industrial Transformation. NJ: Princeton University Press.

Evans, Peter. 1979. Dependent Development: the Alliance of Multinational, State, and Local Capital in Brazil. Princeton, NJ: Princeton University Press.

Francis, Corinna-Barbara. 1997. Commercialization without privatization: government spinoffs in China’s high-tech sector. In Commercializing High Technology: East and West, edited by Judith B. Sedaitis. New York: Rowman & Littlefield Publishers, Inc.

Haggard, Stephan. 1990. Pathways from the Periphery: the Politics of Growth in the Newly Industrializing Countries. Ithaca, NY: Cornell University Press.

Hobday, M. 2001. The electronics industries of the Asia-Pacific: Exploiting international production networks for economic development. Asian-Pacific Economic Literature 15, no. 1:13-29.

Hobday, Michael. 1995. Innovation in East Asia: the Challenge to Japan. Brookfield, VM: Edward Elgar.

Huchet, Jean-Franscois. 1997. The China circle and technological development in the Chinese electronics industry. China circle: economics and electronics in the PRC, Taiwan and Hong Kong. Washington, DC: Brookings Institution Press. 254-289.

Kim, Linsu. 1980. States of development of industrial technology in a developing country: a model. Research Policy 9, no. 3:254-277.

Lall, S. 1984. Transnationals and the third world: changing perceptions. National Westminster Bank Quarterly Review no. May: 2-16.

Lemoine, Francoise and Deniz Unal-Kesenci. 2004. Assembly trade and technology transfer: the case of China. World Development 32, no. 5: 829-850.

Malecki, Edward. 1991. Technology and Economic Development: the Dynamics of Local, Regional and National Change. Essex, UK: Longman scientific and technical.

Naughton, Barry, and Segal, Adam. 2003. China in search of a workable model: technology development in the new Millennium. In Crisis and Innovation: in Asian Technology. Cambridge, UK: Cambridge University Press.

Nelson, Richard R. 1996. The Sources of Economic Growth. Cambridge, MA: Harvard University Press.

Nelson, Richard R. and Winter, Sidney G. 1982. The Evolutionary Theory of Economic Change. Cambridge, MA: Belknap Press.

OECD. OECD Information Technology Outlook: Information and Communication Technologies, 2006.

Porter, W. Philip and Sheppard, Eric S. 1998. The World of Difference: Society, Nature, Development. New York: The Guilford Press.

Rostow, Walt. 1971. The Stages of Economic Growth, a Non-Communist Manifesto. 2nd ed. Cambridge: Cambridge University Press.

Wade, Robert. 1990. Governing the Market: Economic Theory and the role of Government in East Asian industrialization. Princeton, NJ: Princeton University Press.

Webber, Michael J. and David Rigby. 1996. The Golden Age Illusion: Rethinking Postwar Capitalism. New York: Guilford

World Bank Group. ICT and millennium development goals: a World Bank group perspective. 2003].

World Bank. 1993. The East Asian Miracle: Economic Growth and Public Policy. New York: Oxford University Press.

Endnotes:

[1] In 2005, Zhongguancun adopted a new English name: Z-park. The simple name is designed to help ZGC’s international recognition. This article will use its original Chinese name-Zhongguancun (ZGC), which has been associated with the region’s identity the longest in China.

[2] The information communication technology sector is defined by the World Bank as consisting of hardware, software, networks, and media for the collection, storage, processing, transmission, and presentation of information (voice, data, text, images) (World Bank Group 2003, p. 1). Under the Chinese classification system, ICT includes telecommunication equipment, computer and other electronic equipment manufacturing, electronic information equipment sales and leasing, electronic information communication services and computer services and software (National Bureau of Statistics, GB/T 4754-2002). Many services focusing on the ICT industry, such as venture capital, consulting firms, legal offices, and so on, may not be part of the official Chinese statistics on the ICT industry. Accordingly, I include data from other sources.

[3] The Zhongguancun Administrative Committee provides certification for firms that are deemed high-tech enterprises based on R & D inputs, shares of exports, and so on. Those that are certified are exempt from paying corporate income taxes for three years and pay a reduced tax rate for another three years. The review process is supposed to take place annually, and hundreds of firms may lose their status as certified high-tech firms every year. See “Zhongguancun Regulation.”

[4] Income from technology sales includes licensing fees, technological transfer charges, patent fees and income from technical contracts and services. It does not include revenue from selling manufactured goods.

[5] OEM is the dominant system of export in Taiwan and Southeast Asian countries, where the manufacturers in developing countries produce products for multinational name-brand companies to sell abroad.