Three years ago, we published an article in Asia Pacific Journal: Japan Focus on Taiwan’s energy debates and an accompanying article in Taipei Times with the title ‘China key to Taiwan energy crisis’. At the time, Taiwan was embroiled in endless debates over its commitment to nuclear power, a commitment that precluded a shift to more secure renewable energy sources. We argued that Taiwan’s obsession with nuclear power as the way forward in energy policy obscured other options. In particular, the country could extend its great successes in IT, semiconductors and flat panel displays to the next great technological challenge, namely renewable energy. We pointed to the example of China and its green energy strategy which is gradually replacing its black, fossil fuelled strategy, thereby improving China’s energy security as well as building renewable energy industries as export platforms for the future.

Now, three years on, the situation in Taiwan is completely different. There is in place a new President and government, and a new ‘green energy’ strategy. The Democratic Progressive Party (DPP) government led by the first female president in Taiwan, Tsai Ing-wen, elected in January 2016, is taking Taiwan in a new energy direction, headlined by a commitment to be nuclear-free by 2025. That opens the way to an alternative energy strategy, now focused on building Taiwan’s strength in solar PV and offshore wind power. New targets for 2020 and 2025 are providing the investment certainty that the previous nuclear preoccupations had denied. The government is backing its energy targets with talk of total investment of NT$1,500 billion (about US$48 billion), induced initially by government expenditure and then followed by foreign capital and domestic investment. The current power monopoly Taiwan Power (Taipower), with a nod to the new government policy, has already announced an investment target of NT$ 400 billion (about US$17 billion ) in the development of renewable energy (mainly in solar and wind power) in the nine years (up to 2025). So things are on the move on the energy front in Taiwan.

There already are clear indications that the new energy policy is being implemented, even though the government is still in its first year of office. These signals include a moratorium on nuclear power and a commitment to phase it out completely by 2025. In addition, there are new government policies in place to build 20 GW of solar power by 2025 as well as 3 GW of offshore wind power – which on their own would be sufficient to replace the nuclear power plants as they are mothballed. 1 A first step towards this goal is a doubling of solar PV power generating capacity to reach 1.4 GW by 2017. An institutional innovation has been the creation of the Energy and Carbon Reduction Office (ECRO) in Taiwan, established in July 2016, as a means of coordinating green energy initiatives with a view to reducing Taiwan’s carbon emissions.

In this article we review these trends, and discuss the next steps that are needed to enable Taiwan to build on its brilliant manufacturing successes in the fields of ICT, such as flat panel displays, semiconductors, telecommunications and PCs, and extend these in the new renewable energy directions now opening up.2

Taiwan’s current electric power mix and DPP strategy

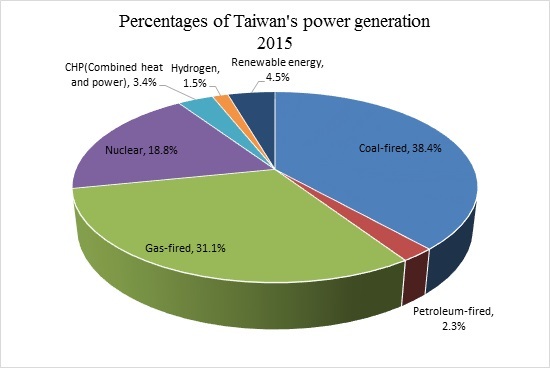

Past commitments to fossil fuels and nuclear by the country’s monopoly power generator Taiwan Power (Taipower), have left Taiwan a laggard in the global shift to renewable energy. Taiwan’s total electric power capacity, from all sources, is 40 GW, or 40 billion watts, compared with the US at 1000 GW and China at around 1,500 GW . In per capita terms, Taiwan’s current power capacity is 1.74 kW per person, compared with 3.1 kW per person in the US and 1.2 kW in China. In 2015, its power generation mix saw coal as the principal fuel (38.4%), followed by liquefied natural gas (LNG) (31.1%) and nuclear at 13.8%. Renewable energy (water, wind and sun) accounted for just 4.5% of power generation (Fig. 1).

|

Figure 1 Taiwan’s electric power generation 2015 (Source: Taipower) |

Expanding the nuclear option has been ruled out by the incoming DPP government, while relying further on coal and LNG is both expensive and a source of energy insecurity because they are nearly 100% imports. So that leaves few options other than renewables as a means of resolving Taiwan’s energy issues. This is both a challenge as well as a huge opportunity.

DPP green energy policy

The DPP under the leadership of Tsai Ing-wen went to the election at the end of 2015 with an energy policy that called for closure of the country’s nuclear power production by 2025 (an approach similar to that of Merkel’s government in Germany), combined with calls for rapid expansion of renewable energy generating sources and enhancement of energy efficiency. The party fought the election with a commitment to reach 20% dependence on renewables for electric power generation by 2025. Since the election there have been some scattered statements, in particular a reinforced commitment to a ‘nuclear free homeland’ by 2025, and a target for solar power of 20 GW by 2025 as well as a target for offshore wind power of 3 GW. On their own these targets would easily make up for the decommissioning of nuclear power stations with a current capacity of 5.1 GW.

The DPP’s green energy policy is viewed as evolving through three stages. The first stage is to integrate green energy-related information and communications technology, materials, machinery, and research resources from both corporate and academic institutions. Such integration includes setting up an energy innovation industrial park in Shalun, Tainan province (located in the Southern Taiwan) with the land size 1118 hectares, or 11.2 km2. (New Energy Association of Taiwan). The park would be designed to act as a hub used to integrate the island’s talents, innovation and technology, and would export products for industrial use overseas. The proposed park would also support the local renewable energy sector, such as offshore wind energy in the Taiwan Strait, solar power in Southern Taiwan, geothermal energy in Yilan (Eastern Taiwan) and ocean/tidal power in the Pacific Ocean (see Figure 2). There would also be a focus on development of energy conservation technologies, in order to constrain energy growth in demand.

|

Figure 2: Geography of targeted green energy development in Taiwan (Source: Green Energy and Environment Research Laboratories and compiled by the authors) |

The second stage of the policy would see a focus on increasing green energy generation as a way to attract NT$1 trillion investment (approximately US$ 31 billion) in related industries — to help turn it into a promising industry while the renewable energy development platform is implemented. The third stage would then be aimed at increasing exports not only of components/products but also turnkey solution/integration systems into international markets, on the assumption that by then the global market for green energy would be more mature.

To overcome the criticism that green energy is a fluctuating (hence non-dispatchable3) source of electricity, the DPP government has also announced plans to increase gas-fired energy as a reserve power source (idle capacity) while promoting energy-saving programs across different sectors. Taiwan is now to build a third LNG terminal, expanding the storage stations and gas-fired plants in order to meet the variations in energy demand when the current three operating nuclear power plants I, II, and III are sequentially decommissioned (as planned) in 2019, 2023, and 2025.

Green energy initiatives and prospects

At this stage the best prospects for Taiwan would appear to be solar photovoltaic (PV) systems and offshore wind. This is because both solar PV and wind power are now mature technologies where Taiwan already has industrial experience and can utilize its ‘fast follower’ strategies to good effect, while investing in R&D to bring it abreast of world leaders.4

Solar photovoltaic

Taiwan, a small, tear-drop shaped island 180 kilometers off the coast of China’s Fujian Province, is the world’s second largest producer of solar cells, shipping 10.6 GW of cells in 2015 – nearly a fifth of the world total of 55 GW. Taiwan is also one of the leading solar wafer and module makers in the world, with well-established firms like Motech, Gintech, Solartech, E-Ton and newcomer TSEC providing a solid industrial value chain. Taiwan’s solar PV production activities got under way around the year 2000, and by 2009 Taiwan was second producer in the world, after China (Fig. 3). Figure 3 also indicates that the production of solar PV in Japan has declined – in line with the sequence of flying geese model as seen in many electronics and information technology industries such as PCs, semiconductors, and flat panel displays. As Japanese production declined, so production in China, Taiwan, and other Asian latecomers increased.

Taiwan’s industrial development body ITRI (Industrial Technology Research Institute) projects the development of a green energy sector in Taiwan moving through successive phases, as technologies and capabilities are mastered. The sector as a whole is foreseen to be worth eventually NT$ 200 billion (US$ 6.3 billion) by 2016 (Fig. 4).5

However, Taiwan’s domestic solar PVs market remains woefully underdeveloped, with accumulated installations adding up to less than 700 MW in 2015 (0.7 GW), accounting for just 2.4% of a total power generating capacity (6 Consequently, the Council of Agriculture (COA) under the Ministry of Interior has released about 1,200 hectares (12 km2) of idle agricultural land and land subsidence for solar development, enough for some 1GW of solar power installation (Taiwan’s Solar PV Forum, 2016).

|

Figure 3. World manufacturing of solar PV panels, by country, 1995-2015 (Source: PV magazine) |

To find more space for installing solar PVs, the government is reported to be working on alternative agricultural practices by developing methods that allow the land to be used simultaneously for both agriculture and solar PV — such as growing mushrooms under the panels, above-the-water or floating solar panels on aquatic farms and other such devices. In addition, dams and ponds larger than 660 m2 are also listed as targets for solar development. There is a subsidy paid for ‘agricultural’ solar PV determined by the formula (designed by the Bureau of Energy, of the Ministry of Economic Affairs) that depends on the power capacity and type of solar PV along with the cost changes of solar PV equipment. In 2016, the Feed-in Tariff (FIT) for solar PV ranged from NT$4.66 to $6.48 (compared to the fossil fuel price of NT$2.85-$2.93).

For better return-on-investment performance, Taiwan’s new government seems to be encouraging the installation of longer duration ground-mounted solar power plants (lasting 20-35 years) rather than the roof-top solar power (which last on average 10-15 years, depending on the lifetime of the buildings). Current data on Taiwan practices is provided by the TSEC company (one of Taiwan’s major solar system companies).7 The solar daily mean yield (DMY) in central and southern Taiwan (which has proved to have the highest levels of insolation across Taiwan) is 4.35 hours, power system efficiency is operating at the average rate of 82%, annual efficiency decay 1%, natural damage ratio 1%, maintenance and repair 21 days/per year, land usage/MW is 1.1 hectares, land rental cost NT$200,000/hectare, feedback fund to the local government is NT$100,000/hectare, bank loan interest rate 2.85% (based on 10 years loan). There are three major capital costs for building a ground-mounted solar power plant, namely infrastructure and construction cost (47%), solar module system (44%), and utility converters (9% with 5-7 duration years). Therefore, the first year capital cost is approximately NT$52,000/kw. Based on whether the solar plants operate for 20/25/30/35 years, the total costs/kw are NT$59,000/$62,500/$66,000/$69,500 respectively while the depreciation cost is greatly reduced as the lifetime is extended. By taking 25-30 depreciation years as a base, the solar PV power generation cost is expected to reach ‘grid parity’ NT$3.17-$3.30/kwh (approximately US$0.1/kwh) and comparable to Taiwan’s current subsidized fossil fuel price (NT$2.85-2.93). These are all promising data for the development of solar power generation in Taiwan.

|

Figure 4. Various targeted energy sectors and their current life cycle stages in Taiwan (Source: ITRI and compiled by the authors) |

The recent announcement of the release of 10,000 hectares (100 km2) for solar development is evidence that the new government seems to be making good on its promise to substantially ramp up the share of power generation by renewables. To squeeze the accessible land (but prevent the trade-off with regular economic activities), some public lands such as sanitary landfill sites have also been designated for solar power plant installation.8

In this connection, the Taipei city government announced in August 2016 that it intended to build its first solar power farm in Taipei at a 37 hectare former landfill, Fudekeng Environmental Restoration Park, using ground-mounted solar panels. The project is contracted with the Taiwan-based Tatung company, one of Taiwan’s leading brands for energy saving systems and services. The solar power plant is expected to be completed by the end of 2016 with the target of generating up to 2 million kilowatt-hours of electricity per year. The Taipei city government is expected to share the utility profit from the feed-in-tariff (FIT) scheme with Tatung and receive approximately NT$1 million annually.9 Currently, renewable energy sources generate about 487 million kilowatt-hours of electricity for Taipei, which accounts for only 3 percent of the city’s total power consumption. The city (which is under separate political control from the national government) is aiming to increase the contribution by renewable energy sources to 10 percent of its total power generation by the end of 2025.

Offshore wind power

To achieve the goal of 3GW wind power by 2025, the government is aggressively implementing the ‘thousand wind turbines’ project utilizing the Taiwan Strait, one of the world’s best offshore wind sites.10 The government closely collaborates with the UK and adopts its “Three Rounds” model for developing the offshore wind power guideline. This follows the sequence with initial demonstration farms (Round 1), then potential shallow areas (Round 2), and finally commercial and zonal deep water development (Round 3) (Higgins and Foley 2014). The development of the offshore wind farms also includes strategic environmental assessments, infrastructure construction, and fisheries compensation negotiations. The Offshore Demonstration Incentive Program aims to complete 4 demonstration turbines by 2015 (progress is currently delayed due to the fact that the fisheries compensation negotiation is not finalized) and three demonstration wind farms by 2020 while the government plans to subsidize 50 % cost of the demonstration turbines (with FIT advances/interest-free loan) and NT$250 million for preparatory and developing processes expenses, according to the report of the Offshore Demonstration Incentive Office. The project forecasts are outlined in Table 1, revealing how the target of 3 GW of offshore wind power is to be reached by 2030.

Table 1: Taiwan’s ‘thousand wind turbines’ project, 2015-2030 projections

|

2015 |

2020 |

2025 |

2030 |

|||||

|

MW |

No. |

MW |

No. |

MW |

No. |

MW |

No. |

|

|

Onshore |

866 |

350 |

1200 |

450 |

1200 |

450 |

1200 |

450 |

|

Offshore |

15 |

4 |

600 |

120 |

1800 |

360 |

3000 |

600 |

|

Total |

881 |

354 |

1800 |

570 |

3000 |

810 |

4200 |

1050 |

Source: Offshore Demonstration Incentive Office, Taiwan

Financing of Taiwan’s green shift

While the technologies and business models supporting a shift to green energy in Taiwan are important, the financing is also a matter of the highest priority. Already in Taiwan in July 2014 there was a sprinkling of Taiwanese interest in issuing green corporate bonds. The country’s then-largest solar cell manufacturer, NeoSolar, issued a corporate bond in July 2014 raising US$ 120 million to expand its green energy manufacturing activities.11 In the same year there was also a corporate green bond issued by Taiwan’s Advanced Semiconductor Engineering (ASE), to facilitate the company’s shift to greener production.

In 2016 there has been renewed activity, led by Chailease Finance Co., one of Taiwan’s finance companies as well as the owner of 31 solar power plants in Taiwan making it Taiwan’s third largest owner of solar power plants. Chailease is expected to issue solar asset backed bonds in 2016, corresponding to a generating capacity of 150MW and a market value of NT$9 billion (approximately US$300 million). The securities are expected to be of 5-year and 10-year duration and are designed to support Taiwan’s developing solar power systems (Energy Trend — in Chinese). The underwriter is CTBC Bank and most of subscribers are insurance companies in Taiwan while all of these assets are 20-year solar power purchasing agreements (PPAs) with Taipower12.

Deregulation of the power sector

Like other East Asian countries, including Japan, Korea and China, Taiwan has inherited a quasi-monopoly power company, Taipower, which could be viewed as an obstacle to further greening. Founded in 1946, it generates power, buys power from a handful of independent power producers (IPPs), distributes power and manages most of the country’s retail and wholesale power activities. There have been many attempts to break the Taipower monopoly, going back at least to 2001 (postponed to 2006) – which came to nothing. Now there is new urgency, since the green power shift is clearly being delayed by the Taipower monopoly.

Reform of the utility regulations would greatly influence the performance of Taiwan’s green energy policy (Wang, 2006). When campaigning for the presidency, Tsai Ing-wen committed her party to review the country’s Electricity Act with a view to introducing greater competition and efficiency.13 As a state-owned utility monopoly, Taipower has long been an economic booster to subsidize the utility prices for electricity supplied to both residential (NT$2.85/kwh, approximately US$0.089/kwh) and industrial (NT$2.93/kwh, about US$0.091/kwh) users. In past decades, this significant subsidy enabled Taiwan to emerge as one of the world’s lowest utility cost countries. Hence reform of the regulation of Taiwan’s utility sector and pricing of electricity, in order to introduce competition in power generation and sale, is now an urgent matter (Chang and Lee, 2016). However, such institutional reforms raise issues of national security as well as the transaction costs for negotiating with both economic and political interests groups such as the Taipower labor union. The Taipower labor union once threatened to strike while pro-nuclear political parties are using media to influence the public opinion. The issues involve preventing ‘privatization of Taipower’ and allowing Taipower to own and establish subsidiaries for power generation, delivery, distribution, sales, and grid networks, all in the name of promoting competition in the power sector. Most recently, in mid-August, the new government reached agreement with the Taipower labor union, making four significant concessions. First, the MOEA agreed to exclude privatization of Taipower from any proposed amendments. Second, within 6-9 years (up to 2025) in two developmental stages, green power is to be directly supplied by Taipower to customers (for the 1st stage) while independent producers in the industrial parks will be allowed to distribute the power produced by their own power plants (for the 2nd stage). In other words, the entities managing power supply and power grid are to be separated. Third, Taipower is to be reorganized as a parent holding company with two subsidiaries for power supply and power grid responsible for distribution, transmission, and sales business. And fourth, any further subsidiaries will be established only if workers’ rights and interests are not adversely affected. Such organizational restructuring of Taipower and deregulation of the power sector are aimed to encourage the dispersal of power sources and micro grid communities.

The new government sees revision of the Electricity Act as key to the deregulation of the power industry and the success of the government’s anti-nuclear-power, development, energy and environmental protection policies. As soon as the concessions were agreed, the new DPP government (facilitated by the Executive Yuan) immediately sent a draft of the ‘Revision of the Electricity Act’ (i.e. the deregulation) to the Legislative Yuan in early September 2016. It is already listed as one of the ‘priority bills’ for the legislature to finalize in the coming session where the DPP is for the first time playing the role of the majority party.14

Smart grid promotion

One aspect of Taiwan’s power system which has not been neglected by Taipower is the shift to a smart grid, or IT-enabled grid that facilitates real-time management and control as a means of saving electricity. There is a worldwide shift underway to build such IT-enabled grids, and Taipower has been one of the foremost players in this endeavour. A “Smart Grid Master Plan” was formulated by Taipower and approved by Taiwan’s Executive Yuan in August 2012, under the previous government (Lin et al 2016). In keeping with Taiwan’s expertise in promoting new industries, a vehicle for government-industry collaboration was created, in the form of a Taiwan Smart Grid Industry Association (TSGIA), bringing together Taiwan’s heavy electrical industry and smart grid-related firms for joint development of smart grid technologies and framing of smart grid standards. A total of 18 smart grid projects have so far been launched, under the guidance of the Ministry of Science and Technology (MoST), the Ministry of Economic Affairs (MoEA), the Bureau of Energy and private companies. The focus has been on the technologies involved in Energy Management Systems (EMS) and Virtual Power Plants (VPPs), both critical elements of smart grid innovations. During the first phase of the project, sales of smart grid components and products have been growing at a rate of 80% per year, to reach NT$ 12.4 billion (US$ 390 million) in 2012. Practical applications are to be taken forward under Phase 2 of the project, utilizing the “Penghu smart grid demonstration project” and the “Integrated Application project for demand response, distributed generation and energy storage”.15 We note that all these developments preceded the advent of the DPP government with its fresh energy strategies; as soon as the Legislative Yuan passes the ‘Revision of the Electricity Act’, the way that smart grid initiatives will be integrated with the new renewables strategies will be a point of great interest.

Challenges and conclusions

While the new government’s determination to end the nuclear power era in Taiwan is clear, there is as yet little evidence of a sustained investment strategy that will drive Taiwan’s energy production and manufacturing industries towards renewable power. But it is worth pointing out that Taiwan has the reserves needed for investment once a clear signal is given. Bank deposits in Taiwan’s banks as a whole have recorded a historical high at NT$40 trillion (approximately US$1.27 trillion) in July 2016, according to the statistics of Taiwan’s Central Bank. This amount does not include the reserves of the insurance companies. The total funds available indicate that Taiwan’s financial institutions have the investment capacity which can be activated when the investment target is clear and verified.

Another immediate question concerns whether the DPP’s anti-nuclear stance will simply lead to more coal being burnt in Taiwan, and carbon emissions rising – as has happened initially in Germany. There is evidence that the new government does not intend to allow this to happen. To better respond to fluctuations in power demand in the future, the new government, apart from building a new gas receiving and reservation station, is also planning to spend NT$50 billion to build four big hydro power batteries (one has been built on the Sun Moon Lake) in other four big dams around Taiwan.To prevent NIMBY (Not In My Back Yard) effects on generation and transmission projects as well as resistance/lassitude concerning efficiency/conservation measures, efforts have also been expended to make power generation choices more transparent. The new government is working with social enterprise platforms such as Code for Tomorrow (equivalent to the US’s ‘Social Coding 4 Good (SC4G)’ and G0v.tw (see http://g0v.tw/en-US/about.html) to encourage the open data and transparent development in the public sector. The goal is to marshal public efforts to provide citizens with easy-to-use information and with easy-to-participate means for discussion of critical social issues such as renewable energy development. Amongst which, the non-confidential database of Taipower such as coal-fired amounts, power consumption by hours, days, seasons, regions, etc. as well as its budget and costs areto be disclosed. All these efforts are aimed to ensure the nuclear-free policy is not traded-off by the increased coal-burning and carbon emissions.

We then conclude by asking what are the difficulties and challenges involved in achieving the non-nuclear goal by 2025 in Taiwan. The first point is the obvious one that the government has been making its initial moves without the benefit of a thorough public airing of the issues. There is an immediate need for a full government-led inquiry into Taiwan’s energy future, where the options for moving beyond nuclear and fossil fuels can be discussed. One of the critical points in such an inquiry would be to draw on Taiwan’s own track record as a high technology fast follower, with an important role for the government industrial laboratories ITRI in this next phase of Taiwan’s industrial development.

Second, new greening programs also call for integration of policies across various government departments and agencies as well as NGOs. Energy administration has become fragmented, with various contributions from different administration authorities, such as the Councils of Agriculture, Interiors, Environmental Protection, and Ministry of Economic Affairs, working at cross-purposes. Third, funding arrangements need clarification. Investment strategies and fundraising mechanisms at the initial stage are not clear yet. Fourth, the compensation and negotiation mechanisms are not legally guaranteed. The lack of a secure legal framework threatens to increase the time and cost of negotiation activity with stakeholders (such as shifting land use arrangements).

We believe Taiwan could be an important player in renewable energy. For years it has been missing opportunities due to the focus on nuclear power and fossil fuels (which probably owed more to Taiwan’s geopolitical situation than to strictly energy-related concerns). But now the way is open to build the country’s generating capacity utilizing renewables whose impact can be increased by investment in smart grids. This would allow Taiwan to complement its manufacturing capacities in producing solar PV cells as well as (potentially) wind turbines and other renewable energy devices. This is truly a strategy grounded in “building energy security through manufacturing”.16 Taiwan has well-tested industrial development models involving the promotion of new industries through market stimulation and domestic technology leverage, and now is the time to apply these skills to the urgent needs of cleaning up its energy system and creating new pillar industries for the future.

Related articles

John A. Mathews, China’s Continuing Renewable Energy Revolution – latest trends in electric power generation

John Mathews and Hao Tan, The Revision of China’s Energy and Coal Consumption Data: A preliminary analysis

Andrew DeWit, Japan’s Bid to Become a World Leader in Renewable Energy

John Mathews and Hao Tan, A ‘Great Reversal’ in China? Coal continues to decline with enforcement of environmental laws

John A. Mathews and Hao Tan, The Greening of China’s Black Electric Power System? Insights from 2014 Data

John A. Mathews and Hao Tan, “China’s Continuing Renewable Energy Revolution: Global Implications”

John A. Mathews and Hao Tan, “Jousting with James Hansen: China building a renewables powerhouse”

John A. Mathews, The Asian Super Grid

Andrew DeWit, Japan’s Energy Policy at a Crossroads: A Renewable Energy Future?

Sun-Jin YUN, Myung-Rae Cho and David von Hippel, The Current Status of Green Growth in Korea: Energy and Urban Security

Mei-Chih Hu and Ching-Yan Wu, Concentrating Solar Power – China’s New Solar Frontier

References

Chang, C. S. 2016. Presentation to Taiwan Solar PV Forum, Academia Sinica, Taipei, 22 Feb 2016 (in Chinese).

Chang, C.T. and Lee, H.C. 2016. Taiwan’s renewable energy strategy and energy-intensive industrial policy, Renewable and Sustainable Energy Reviews 64: 456-465.

Higgins, O. and Foley, A. 2014. The evolution of offshore windpower in the United Kingdom, Renewable and Sustainable Energy Reviews, 37: 599-612.

Lin, C.Y. 2016. Strategy for ‘nuclear-free homeland’ in Taiwan. Green Energy and Environment Research Laboratories, Industrial Technology Research Institute, Taiwan (in Chinese).

Lin, F.J., Chen, Y., Lu, S.Y. and Hsu, Y. 2016. The smart grid technology development strategy of Taiwan, Smart Grid and Renewable Energy, 7: 155-163.

Mathews, J.A., Hu, M.-C. and Wu, C.-Y. 2012. Fast-follower industrial dynamics: The case of Taiwan’s Solar PV industry, Industry and Innovation, 18 (2): 177-202.

Mathews, J.A. and Tan, H. 2014. Manufacture renewables to build energy security, Nature, 513 (11 Sep 2014): 166-168.

Wang, K.M. 2006. The deregulation of Taiwan electricity supply industry, Energy Policy 34 (16): 2509-2520.

Wu, C.-Y. and Mathews, J.A. 2014. Knowledge flows in the solar photovoltaic industry: Insights from patenting by Taiwan, Korea and China, Research Policy, 41: 524-540

Notes

Taiwan has three nuclear power sites in operation. A fourth nuclear power plant was completed in 2015, but it was mothballed as soon as the construction was finished due to social pressure for a ‘nuclear-free homeland’.

For our earlier articles on Taiwan and renewables, see Mathews, Hu and Wu (2012), and Wu and Mathews (2014).

A source of electricity is considered dispatchable if it can be turned on or off in order to meet changing demand.

In our article three years ago we endorsed concentrated solar power (CSP) systems, involving arrays of lenses and mirrors, but this option did not prove to be a strong contender in Taiwan where industrial strategy is focused on the already well-established and promising solar PV sector. For an overview of recent developments by the Ministry of Economic Affairs, see Pat Gao, ‘A sustainable vision’, July 1 2016, Taiwan Today.

In 2015, the production value of solar PV cells in TW reached NT$170 billion. The goal for NT $200 billion for PV and other renewables is set for 2016.

Some optimistic solar companies such as TSEC investigated the available lands across Taiwan and proposed the goal for 40 GW grounded solar power plants (with 30 years depreciation) by 2030 (Taiwan’s solar PV Forum, 2016).

The data were released by TSEC at Taiwan’s Solar PV Forum held by the Academia Sinica, Taipei, on the 22nd February 2016.

There are 371 landfill sites across Taiwan; 67 sites are under operation and 250 sites are in ecological restoration

According to the database investigated by the British marine consultancy, 4C Offshore Company, for the global wind farms, Taiwan Strait secures 16 best sites out of the 18 world’s best wind farm sites.

See the Bloomberg story ‘Chailease Plans Solar-Backed Bonds on Taiwan Clean Power Push’, August 24 2016.