Abstract

Prime Minister Abe has committed 3 trillion yen ($27 billion) to finance a linear Shinkansen project linking Tokyo and Nagoya/Osaka by Maglev. Technical analysis shows that the Linear Shinkansen constitutes not only an extraordinarily costly but also an abnormally energy-wasting project, consuming in operation between four and five times as much power as the Tokaido Shinkansen which already provides high speed rail connection. Since the 1960s, Japan’s major construction projects have become vastly more costly and less efficient. Deficit-breeding, energy-wasting, environmentally-destructive, and technologically unreliable, the Linear Shinkansen project must be considered a guaranteed fiasco, with the potential not only of its own collapse but of bringing the Tokaido Shinkansen down too.

Keywords: Linear Shinkansen, Maglev, Construction State, Primary Energy Supply, Total Industrial Output

1. Linear Shinkansen: Upgrade to National Project

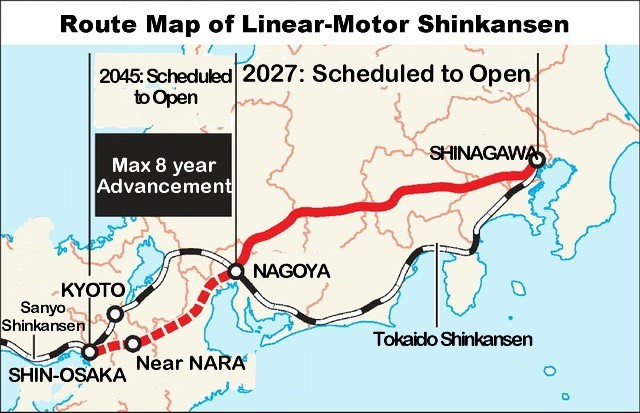

On August 2, 2016, Japan’s Prime Minister Abe Shinzo and his cabinet decided on 28.2 trillion yen worth of economic measures described as an “investment for the future”. Included was ca. 3 trillion yen ($27 billion) in financial assistance to Japan Rail Tokai’s Linear Shinkansen project.1 That massive infusion of public funds would allow the acceleration of completion date by 8 years, from 2045 to 2037.

The Linear Shinkansen plan is a project to connect Tokyo-Osaka (438 kms) in 67 minutes by magnetically levitated (superconducting maglev.) bullet trains, with a maximum speed of 505 km/h and for a total cost estimated at 9.03 trillion yen. The first stage object is to start service on the Tokyo-Nagoya 286 kms sector by 2027, for an investment of 5.43 trillion yen. Overall completion of the line through to Osaka, under the revised Abe government plan, is to occur in 2037.2

|

Route Map of the Linear Shinkansen |

At the Ise-Shima G7 Summit in May 2016, Prime Minister Abe, claiming that the world economy was on the brink of deflation, requested participant countries to take fiscal stimulus fiscal policies in line with Japan. The fact that he proposed such an extraordinary fiscal spending package right after this G7 Summit suggests that the Linear Shinkansen project may be seen as the centerpiece of his fiscal policy.

|

The Linear Chūō Shinkansen |

Despite its gigantic scale, the Linear Shinkansen project has attracted little public attention. This is probably due to the fact that the direct benefits of the project are confined to passengers who want to travel between Tokyo and Nagoya/Osaka, already well served by Shinkansen, at ultra-high speed. Notwithstanding such reservations on the part of the public about the project, Prime Minister Abe decided to upgrade the Linear Shinkansen from a mere private sector construction investment to a “state project.” Abe’s second term [from December 2012] cabinet attached highest priority to “economic resurgence” and the prime minister declared his economic policies, labeling them “Abenomics.” They combined three elements.3

(a) Increased fiscal spending to stimulate the economy

(b) Liberalization and deregulation of labor markets in order to reinforce global competitiveness, and

(c) Monetary relaxation by the Bank of Japan, on an “unprecedented scale,” in search of a 2 per cent inflation rate.

They became known as his “Three Arrows.”

Let us reconsider, historically, trends in stimulus policies since the bursting of the asset and equities bubble in 1990.

(1) First, resumption of traditional spending based on Keynesian principles and in accord with the distinctive Japanese construction sector priority

(2) Then, beginning in the 21st century, a drastic switch to neo-liberal, market fundamentalist policies, under which economic revival was left to market principles and labor protection regulations scrapped as impediments to “liberal” business activity. Wage cutting and employment instability followed, resulting in worsening income inequality.

The (a), (b) and (c) of “Abenomics” called for the simultaneous adoption of (1) and (2), while seeking policy adjustments by means of (c) monetary relaxation by the Bank of Japan on an “unprecedented scale.” However, upon closer consideration, fiscal spending corresponding to Abe’s (1) and (a) was unable to restrain the buildup of enormous fiscal deficits. Recognizing this, a switch to (2) and (b) to enhance market competitiveness became necessary despite widening and intensifying income inequality. Extraordinary monetary relaxation (c), even by resort to prolonged negative interest rates, did little to boost investment but resulted in an enormous abnormal accumulation of internal corporate reserves (idle capital). In short, Abe’s policy mix of (a)+(b)+(c), amounts to a repeat of the failure of (a)+(b).

Mainstream economists generally seem to hold it as axiomatic that economic stagnation is a temporary and abnormal aberration from the normal, persistent growth economy and that the “normal” trajectory can be resumed provided that the government makes appropriate economic policy settings. This theory is almost universally followed by the Abe cabinet, by bureaucrats associated with government including Bank of Japan officials, and, especially, by academics who provide the theoretical framework for policy.

This dogma should have collapsed long ago. Economic growth post-1945 reached its limit (at least in the Northern hemisphere) by the 1990s or at least by the end of the 20th century, and has undergone transition to saturation-stagnation. If so, promotion of the policy (a) will result in very ineffective investment so far as resources, energy and fiscal policy are concerned.

Prime Minister Abe, having won a landslide victory in the July 2016 Upper House election, proclaimed that he would further promote “Abenomics.” Fiscal assistance to the Linear Shinkansen became part of his policy. It is necessary to examine whether the Linear Shinkansen and Abenomics in general can achieve results to match such investment. To do this, however, a more fundamental review and analysis on the historical progression of Japan’s economy as a whole is called for.

2. Historical Correlation between Primary Energy Supply and Total Industrial Output

First, let us discuss the historical changes of Japan’s Primary Energy Supply (PES) and Total Industrial Output (TIO) as shown in Fig.2 and Table 1. Japan’s Primary Energy Supply grew by an extraordinary ca 6.5 times (equal to 9 per cent per year) or from ca. 60 million TOE (Tons of Oil Equivalent) to ca. 400 million TOE in the two decades from the early 1950s to 1973, the year of the First Oil Crisis. Primary Energy Supply then (in 1973) suddenly halted at around 400 million TOE and went into a temporary plateau. From 1983 it resumed a slow expansion, reaching a second plateau of around 500 million TOE from 1990.

Over the 40 years from 1973, Japan’s Total Industrial Output (in terms of nominal yen) began to rise very rapidly, following a time lag of ten years or so after the rise of Primary Energy Supply. This time lag, we consider, was due to the structural correlation between rise in Primary Energy Supply and Total Industrial Output growth. In other words, the drastic prior expansion of Primary Energy Supply was the necessary precondition for the drastic expansion of Total Industrial Output in post-war Japan. As shown in Fig. 2, the surprising rise of the Primary Energy Supply suddenly and entirely ceased at the time of the First Oil Crisis in 1973.

In contrast to PES’s loss of key role, Japan’s Total Industrial Output survived this oil shock and continued to rise for the following two decades, further prolonging the time lag against rise in Primary Energy Supply. However, Total Industrial Output then seems to have exhausted its growth potential, first gradually during the financial bubble in the late 1980s, then precipitously, as the stock and land price bubble burst in 1990. Subsequently, both TIO and PES hit a very similar ceiling of around 1000 trillion yen and 550 million TOE (for PES),

This figure clearly shows that the dual but time-sequential expansion of Primary Energy Supply and Total Industrial Output must have been a one-off, monocarpic historical process. Japan’s once marvelous growth of the PES-TIO combination must have ended forever.

|

Total Primary Energy Supply, Total Industrial Output and Gross Domestic Product of Japan, 1955-2011 |

|

Historical Shifts in Japan’s Primary Energy Supply, Total Industrial Output, and Gross Domestic Product (Numerical Resume) |

3. The Business Structure of the Linear Shinkansen Plan

To estimate the actual business structure of the Linear Shinkansen, let us compare it with the Tokaido Shinkansen that opened on October 1, 1964, just 10 days before the opening ceremony of the Tokyo Olympics. This line, well-known as a global trailblazer of the high-performance intercity express, has a span of 515 kms. Total construction cost was 380 billion yen, of which 28.8 billion yen (80 million dollars) was supplied by the World Bank (at the then exchange rate of: 1USD=¥360).

Japan also now has one functioning linear-line, called LINIMO, i.e., the Aichi High-Speed Transit Tobu Kyuryo Line built to service the 2005 Nagoya Expo. Its trains are magnetically levitated and driven by normal-conductive (not superconductive) coils. This tiny (9 km) line cost 100.8 billion yen, nearly equivalent to 900 million dollars (at the 2005 exchange rate of ¥110/USD. Astonishingly, its cost was roughly equal to the total cost of the Tokaido Shinkansen (approximately 1.06 billion dollars when calculated at the 1960s rate of ¥360/USD).

Table 2 compares these two earlier railway projects and the Linear Shinkansen.

|

Comparison of the Linear Shinkansen and the Two Previous Railway Projects |

As shown in Table 2, the total cost of the Tokaido Shinkansen would be 1.6422 trillion yen, if rendered in the current price on the basis of the CPI (consumer price index). The Linear Shinkansen is estimated to cost at least 9.03 trillion yen, or about 5.5 times more than the Tokaido Shinkansen. If we use the CGPI (corporate goods price index) with 2010 as 100, the Tokaido Shinkansen’s original (1964) cost of 380 billion yen will become 803.4 billion yen, which is yet substantially lower than the CPI-based conversion, and the Linear Shinkansen’s cost is 11.3 times greater.

The Linear Shinkansen’s unit cost is estimated at 20.6 billion yen per km, compared to the 3.2 billion yen per km or less for the Tokaido Shinkansen, For a more meaningful comparison, some recent subway construction may be considered, for example, the Fukuoka Municipal Subway’s Nanakuma Line which opened in 2005 at an estimated cost of 282.9 billion yen, or 23.57 billion yen per km for the 12.0 km line.4

The Linear Shinkansen is to have a route distance of 438 kms, nearly equal to the total length (434 kms) of the Tokyo (304 kms) and Osaka (129.9 kms) subway lines.5

4. A Reconsideration of the Importance of Energy Content Value (ECV) in the Case of Three Railway Projects

Having compared the business structures of the new and old Shinkansen projects in terms of monetary value, the problem arises of how to set the conversion rate, since past business has to be recalculated in terms of present-day prices. The results, however, will be greatly affected by the choice of conversion-rate. The fact that the Consumer Price Index (CPI) is about twice as large as the Corporate Goods Price Index (CGPI) means that there will be serious inconsistencies in estimates of the current cost/value. Yet there is no exclusively “correct” criterion on which to base choice.

This suggests the need for a more general and reliable standard for evaluation of economic substances. We propose a novel evaluation standard which we term “Energy Content Value.” which constitutes the Built-In Energy Equivalent (BIEE). This concept, ECV, represents the value of goods or services in terms of the total energy input ’embodied’ in them directly and indirectly.

By way of illustration, let us consider the instance of the electric power industry in Japan: consumers pay, on average, ca. ¥21 for the electricity (energy) of 1kWh.6 However, the actual cost of the primary energy (fossil fuels, enriched uranium, etc.) required to generate 1kWh is approximately ¥8, i.e. 40 percent of the power price. The greater part, ca. 60 per cent, of the power rate is paid for the energy indirectly exploited for the construction and maintenance of equipment and facilities (including power losses during transmission and transformation) and for management and manpower.

Thus it is almost self-evident that 1kWh of electricity “contains” much hidden or “embodied” energy. The ¥21 per kWh power rate must cover the costs for all the energy (i.e. energy content) required for making the 1kWh of power. This power rate (the nominal price) may continually fluctuate due to various conditions including fuel market prices, the yen/USD exchange rate etc. Yet despite such fluctuation, the energy content will remain fairly constant in as much as the systems for energy conversion have been kept stable. In the case of electricity or any other energy product, it is rather easy to be aware of the indirect energy requirements accompanying the energy product (the energy quantity representing the direct part). As for general economic goods and services, they are entirely lacking any representation for the required energy input whether direct or indirect.

Therefore, it is in effect impossible to assign a precise amount of ECV to respective economic goods and activities. However, if we take a synoptic view, a national economy as a whole is materialized by the total Primary Energy Supply (PES). Their correspondence is 1 to 1: the economy cannot obtain any energy except from the PES and all the PES is used within the economy.

In fact Japan’s TIO, ca. 1000 trillion yen, has been materialized by the PES of ca. 500 million TOE for this decade or more. On the basis of this fairly stable circumstance, it will be reasonable to presume the level of the Energy Content Value (ECV) as two million yen per TOE. Some, though not all, industries, such as the electric, the electronic, or transportation industries, materialize their ECVs with explicit energy consumption.

On the basis of such considerations on the concept of ECV, let us review the problems concerning the power industry in Japan. According to the International Energy Agency (IEA), demand from Japan’s power industry accounts for about 40 per cent of Primary Energy Supply.7 The vital importance of the power industry in the nation’s economy is clear. Therefore the complementary relationship between Energy Content Value and monetary value in this sector may be extended to the national economy as a whole. It is based on the PES-TIO relationship shown in Table 1. The ratio, TIO/PES or PES/TIO (shown in Table 1) gives respectively unit cost or unit yield of Energy Content Value’s unit cost or unit yield for the national economy.

Reconsidering the comparison between the three railway projects – Linear Shinkansen, Tokaido Shinkansen, and LINIMO – in terms of the Energy Content Value; we obtain the following results (Table 3).

|

Energy Content Value Comparison between the three railway projects of Linear Shinkansen, Tokaido Shinkansen, and LINIMO |

Technical analysis has already shown that the Linear Shinkansen constitutes an abnormally energy-wasting (low efficiency) project, consuming in operation between four and five times as much power as the Tokaido Shinkansen.8 It is also the case that, at the construction phase prior to operation the Linear Shinkansen will consume seven times as much Energy Content Value (=10893 TOE÷1562 TOE) as the Tokaido Shinkansen in the course of the construction. And the provisional cost estimate for the Linear Shinkansen is a minimum possible, since the costs of such project budgets are conventionally underestimated.

Thus the Linear Shinkansen turns out to be a project of unprecedented absurdity, massively wasting energy even at the construction stage.

5. The Linear Shinkansen Cannot Serve as a Leading Investment

In his intensive analysis on the feasibility of the Linear Shinkansen plan, Hashiyama Reijiro considered three aspects: economic feasibility, technological reliability, and environmental appropriateness. He concluded that it was deficient in all three. In short it was a foolhardy project.9 By way of contrast, Hashiyama gave three examples of “successful” projects that met all three criteria: the Tokaido Shinkansen (opened in October 1964); the Meishin (Nagoya-Kobe) Expressway (opened in July 1965) and its extension, the Tomei (Tokyo-Nagoya) Expressway (opened in May 1969); and the Kurobe Dam (completed in June 1963).10 Subsequently, large public construction projects in Japan became more and more costly and brought less and less benefit, so these cases may be considered fortunate exceptions in Japan’s modern economic history.

Japan’s economy between about 1960 and 1973 had been a focus of international attention for its remarkably high growth performance (7 per cent per annum in real terms). But what deserves even greater attention is that a truly dramatic expansion in productivity (TIO and GDP) occurred in the 1970s and 1980s. It was preceded by a truly miraculous expansion in primary energy consumption, as shown in Fig. 2.

These three successful projects noted were all carried out in the 1960s, effectively providing the infrastructure for more effective transportation and power supply and enabling the next-stage of TIO and GDP growth in the 1970s and 1980s. The resultant growth afforded ample returns on the earlier investments in basic infrastructure such as dams, expressways, and the (Tokaido) Shinkansen.

By contrast, the investment in the Linear Shinkansen is going to be enforced at a time when demand has peaked, constraints on energy supply are severe, and it is inconceivable that the energy to be needed for this project can be supplied from existing energy sources. Promotion of this project will inevitably encroach on existing energy demands. Thus its effect on TIO or GDP is likely to be not suppressive, not expansive.

Furthermore, JR Tokai’s own president admits that there is absolutely no way that the Linear Shinkansen could be a paying proposition.11 Evidently the company entertains no hope of collecting the enormous sums of capital investment, and plans to recover the deficits of the Linear Shinkansen with the profits from the Tokaido Shinkansen. This implies that the Linear Shinkansen (hyper-express) passengers are to be subsidized by the Tokaido Shinkansen (super-express) passengers. JR Tokai management ignores the principle that the recipient of a benefit should pay for it.

From whatever angle one considers it, the Linear Shinkansen fails the test of a leading investment. If JR Tokai is dreaming of the new Linear Shinkansen being a rerun of its past success story (the Tokaido Shinkansen), it is suffering a disastrous misapprehension.

6. Conclusion: The Linear Shinkansen as an Immense Governmental Squandering

How should a government deal with such a major matter as a maglev train system? Germany, for example, once tried to set up a construction project for a maglev system. The government in 1994 approved a special consortium for the Berlin-Hamburg line (292 kms) by Thyssen, Siemens, and Daimler but immediately after the first cabinet decision, it prudently submitted the project to the Ministry of Transportation’s Scientific Advisory Committee. That committee raised serious concerns about the plan’s feasibility, especially in its estimates of demand. Federal Congress adopted a special “Magnetically Levitated Railway Demand Law” and recommended the government reconsider the project.12 Finally in 2000, they canceled it.

On the other hand, Switzerland gave a provisional go-ahead for construction of the Gotthard Base Tunnel (57km) to connect Switzerland and Italy through the Alps. However, the actual construction was permitted only after submission to a national referendum in 1992 following a detailed explanation by the government. It took 17 years to build, at a cost of about $1.6 billion.13 Its maximum speed is 250 km per hour, as compared to Linear Shinkansen’s 505 km per hour. The line eventually opened on June 1, 2016.14

In contrast to these countries, Japan’s politics and administration seemed to have been imprudent or even reckless. The Linear Shinkansen Plan is an enormous project, involving excavation of tunnels up to 310 km in length, likely to have a serious impact on the nation’s economy and environment. Yet Prime Minister Abe, in search of a major stimulus to the stagnant economy, hurriedly decided to inject fiscal funds into it. Furthermore, although it had hitherto been forbidden to apply the Fiscal Investment and Loan provisions to a private company such as JR Tokai, the Abe cabinet ventured to amend the FIL law to make such funding possible.15

Abe’s decision to loan an immense sum under the Fiscal Investment and Loan (FIL) program reminds us of many historical cases of similar fund abuse. The prime example is the application of such funds to clean up the immense loss piled up by the former (state-owned) Japanese National Railway Corporation, irresponsibly passing the long accumulated deficit to the taxpayers.

The FIL program (now restructured into the “Fiscal Investment and Loan Bond”) has long been financed by the nation-wide saving systems: postal savings, postal life insurance, pension reserve fund. The ultimate root of the FIL system may be traced to the public saving system for financing industrial development in the Meiji Era and then for covering Japan’s immense war expenditures for the Sino-Japanese War, the Russo-Japanese War, and finally for World War Two.

In the Second World War, Japan experienced thorough and devastating defeat and total state bankruptcy, yet the national savings system survived essentially intact, and was rebuilt and even reinforced by the post-war government. Together with central and municipal government budgets, the FIL program budgets made up one of the key fiscal institutions referred to as the “Fiscal Trinity.” This system enabled Japan to invest in public works on a scale unprecedented in world history. The FIL constituted the indispensable source of funding for all large-scale public works such as dams, railways, roads, bridges, tunnels, air- and sea-ports.

However, this system was often lax and prodigal, with the result that huge debt accumulated. By April 1987, when the Japan National Railway Corporation was privatized and reorganized into seven Japan Railway companies, it had run up a staggering deficit of 37.1 trillion yen, which included a bad debt of 19.2 trillion yen from the Fiscal Investment and Loan Fund.16

This extraordinary debt was accumulated by improper reliance on the FIL, yet it was that same FIL that was then assigned to cover the deficit. The bulk of the debt was transferred to FIL-compatible special companies, newly set up by the government: the JNR Settlement Corporation (liable for 25.5 trillion yen) and the Shinkansen Holding Corporation (liable for 5.7 trillion yen). The residual debt, 5.9 trillion yen, was transferred to newly established JR East, JR Tokai, JR West, and JR Freight.17 JR Tokai’s share was just 0.3 trillion yen.18

However, by 1998, the deadline initially imposed on the company, the JNR Settlement Corporation that took over two thirds of the total JNR debt (ca. 25 trillion yen) became unable to make any further repayment. Worse, between 1987 and 1998 the JNR debt swelled to 28.3 trillion yen, of which ca. 25 trillion yen was finally transferred to the nation. The still remaining liabilities, comprising future pension liabilities and other businesses handed over from all the JR-related companies, were finally transferred to the Japan Railway Construction Corporation (now the Japan Railway Construction, Transport & Technology Agency).19

Paul Krugman once provided an affirmative comment on Japan’s fiscal policy, saying that “in the early 1990s, Japan boosted its economy by a flood of public investment.”20 But actually this “flood of public investment” had its root in the nation’s long established fiscal policy and it was precisely such reckless spending that led to the bankruptcy of the Japan National Railway Corporation and the resultant irresponsible transfer of its debts to the people. Now the Abe government is about to follow the same course, again injecting FIL funds to Japan Rail Tokai.

Another economist, Joseph Stiglitz, also commented in similarly positive vein that “the Three Arrows of Abenomics, i.e. financial easing, relaxation of fiscal spending, and growth strategy, is the correct policy combination to restore “Japan’s economy.”21 Could he still hold that affirmative position if he realized all the inconsistent aspects of Abe’s economic policy, and if he came to know that a centerpiece of Abe’s newest growth strategy (the Third Arrow) is now the Casino-Resort Bill?22

The Linear Shinkansen is bound to end in failure. The ultimate problem lies in the contradiction that the Linear Shinkansen (a subsidiary) is bound to encroach upon the passengers, the sales, and the profits of the extant Tokaido Shinkansen (the parent). JR Tokai’s Tokaido Shinkansen (the host) was built at a simple cost of 0.38 trillion yen, but the Linear Shinkansen, a parasitic behemoth, is set to devour the huge sum of 9 trillion yen (or possibly more).

There are some, though very few, reliable analyses of the Linear Project, such as the writings of Hashiyama Reijiro and the “Network of Neighborhood Residents along the Linear Shinkansen Route,” yet general public indifference is tantamount to support for the project.

How did such a dubious project come to be adopted as a leading promoter of growth? The first reason is the imprudent enthusiasm for an immense investment regardless of financial feasibility. The magnificent scale of the Project itself stirred up “Linear Fever” and illusory expectations in the Abe administration. This extravagant and comprehensively problematic project came to be seen as promising to restore Japan to growth, even though the plan will turn out to be a heavy burden not only on growth, but even on the sustainability of the nation’s economy. Equally important is the second reason: a naïve (illusory) faith in “advanced technology’’ and its assumed miraculous productivity. This is widely entertained among ordinary people as well as specialists in various fields – politicians, bureaucrats, economists, engineers, scientists etc. This technology fetishism can be associated with the permissive indifference to this project by the general public.

In reality, however, there are plenty of examples to demonstrate the essential vulnerability of so-called “advanced technology.” Recently Toshiba Electric teeters on the verge of bankruptcy due to its suicidal mega-investment in Westinghouse Nuclear Power. Tokyo Electric (TEPCO) also suffered fatal damage from the simultaneous explosions of four nuclear plants in Fukushima, and the accident in Chernobyl was even more disastrous. NASA lost two space shuttles (out of seven) due to catastrophic explosions. The supersonic jetliner Concorde exploded in public view on a runway of De Gaulle Airport in 2000, eventually putting an end to supersonic air travel. Likewise the linear motor trains, driven by superconducting coils and running in super-long/super-deep tunnels, are susceptible to disastrous accident. “Advanced technology” often means high intrinsic risk.

In contrast to these examples, the semiconductor electronics industry seems to be continuing its almost miraculous development. However, this is not a typical but a greatly exceptional case among the advanced technologies. It can even be considered to be part of “traditional technologies” such as the material, chemical, or auto industry. Biotechnology also seems to retain a great potential for development, although it remains questionable whether it can cope with the prevalent biological damages brought by technological civilization.

The deepest problem of the Linear Shinkansen project lies in its financial frailty. JR Tokai maintains a posture of reckless courage while other large-scale companies in general are very cautious about profitability of their investments and tend to prefer internal reserves over dubious capital investment. We conclude from our analysis of JR Tokai’s rather unique behavior that multiple problems converge on this project.

Yet the mass media exaggerate and irresponsibly hail the “economic effects” to be expected from it. The business community and municipalities along the route seem naively to be anticipating economic benefits and to be taking few if any precautions against the negative economic spiral that it might cause.

The Linear Shinkansen problems will inevitably have far-reaching effects not only on government and fiscal policy in general but also on transportation, resources, energy, and environment sectors, yet scholars, academics, researchers and technological experts are largely indifferent, their irresponsible apathy signifying de facto support for the project.23

Deficit-breeding, energy-wasting, environmentally-destructive, and technologically unreliable, the Linear Shinkansen project must be considered a guaranteed fiasco, with the potential in future not only of its own collapse but of bringing the Tokaido Shinkansen down too. Yet this plan has become Japan Rail Tokai’s supreme command and the object of its all-out investment.

The consequences of a huge failure of this nine trillion yen project will inevitably reverberate well beyond JR Tokai itself through Japan’s economy as a whole. The plan to construct the Linear Shinkansen should be treated on the same stage as the reckless plan to restart nuclear plants on known fault lines, setting aside the lessons of the Fukushima disaster. Both spell disaster for the Japanese people.

Related article

- William Steele, Constructing the Construction State: Cement and Postwar Japan

Notes

Jiji, “10-year count-down begins for launch of Tokyo-Nagoya maglev service,” Japan Times, January 9, 2017.

Hashiyama Reijiro, Rinia Shinkansen – kyodai purojekuto no ‘shinjitsu’,” Tokyo, Shueisha, 2014, p. 19. On the revised railway construction plan of August 2016, see “JR Tokai ga tetsudo, unyu kiko ni rinia yushi o shinsei, zaito de 3 cho en, enshin maedaoshi e,” Sankei Shimbun, November 18, 2016.

In 2015, the Abe Government promulgated the ‘Law for Protection of Specified Secrets’ to strengthen state control over information and re-interpreted Article 9 of the Constitution so as to be consonant with the right of collective self-defense. It also steamrollered through the Diet a series of security-related laws, enabling the overseas dispatch of Japanese troops. Abe’s arbitrary and authoritarian lawmaking strongly suggests that his ultimate aim might consist not in reinforcement of the national economy but in restoration of an ultraconservative regime ideologically oriented to Meiji Constitution. (cf. Sugano Kan, Nihon kaigi no kenkyu, Tokyo, Fusosha, 2016).

On the basis of average price rates by the ten power corporations, authors estimate the power rate at 25.51 for home use and 18.86 for industrial use.

Abe Shuji, “Enerugi mondai to shite no rinia shinkansen,” Kagaku, Vol. 83 No. 11, Tokyo, Iwanami, November 2013, pp. 1290-1299.

Hashiyama, Rinia Shinkansen, op.cit. See also Hashiyama Reijiro, Hitsuyo ka, rinia shinkansen, Tokyo, Iwanami, 2011.

“Rinia yushi e kaiseiho seiritsu, zensen kaigyo, saidai 8 nen maedaoshi,” Nihon Keizai Shimbun, November 11, 2014.

Misumi Masakatu, “Choki ni watari shokan ga tsuzuku – ippann kaikei shokei saimu,” Keizai purizumu, No. 48 November 2007.

The Abe cabinet had been treating the Trans-Pacific Partnership (TPP) as the central policy for its growth strategy. As the TPP prospect faded with the rise of Donald Trump in the US, Abe’s ‘last resort’ is the ‘Integrated Resort’ type development in which the casino is to play the leading role. On December 3 2016, the Diet passed the Integrated Resort Law forcibly and almost without Diet discussion.

Hashiyama Reijiro and Abe Shuji, together with movements such as the “Network of Residents along the Linear Shinkansen Line” that has launched a suit for cancellation of the project, constitute exceptions.